Photographer: mbolina/Getty Images/iStockphoto

The Bank of Japan’s High-Wire Act

Central bankers across the developed world are either on the road to tightening monetary policies or speaking about how they plan to do so. Not in Japan, where the economy still depends on monetary stimulus and central bank Governor Haruhiko Kuroda fears talk of removing it would rattle markets and undermine his quest to kill deflation once and for all. And who can blame him? Massive market imbalances fueled by years of asset purchases mean his exit path will be fraught with danger. A misstep could send the economy sliding.

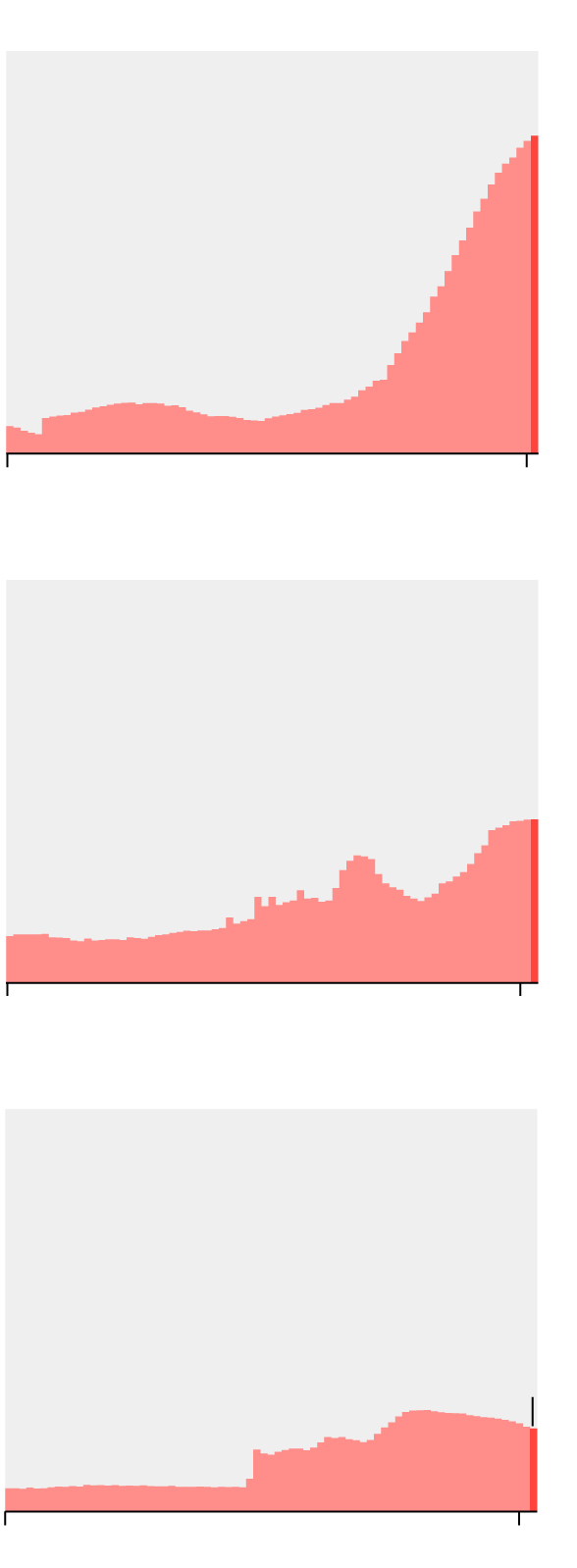

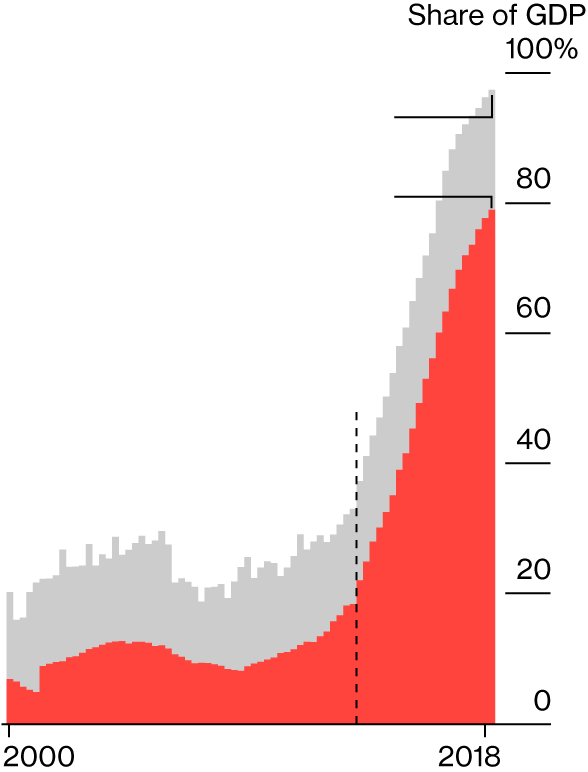

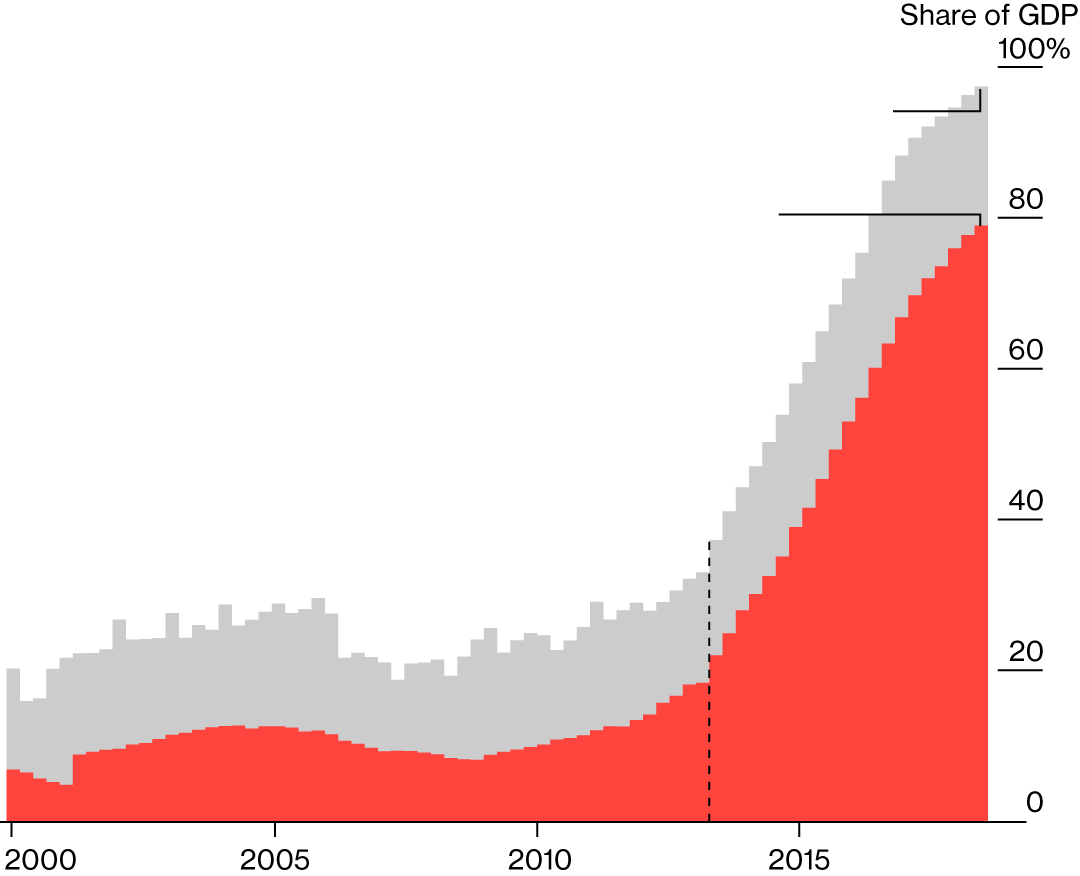

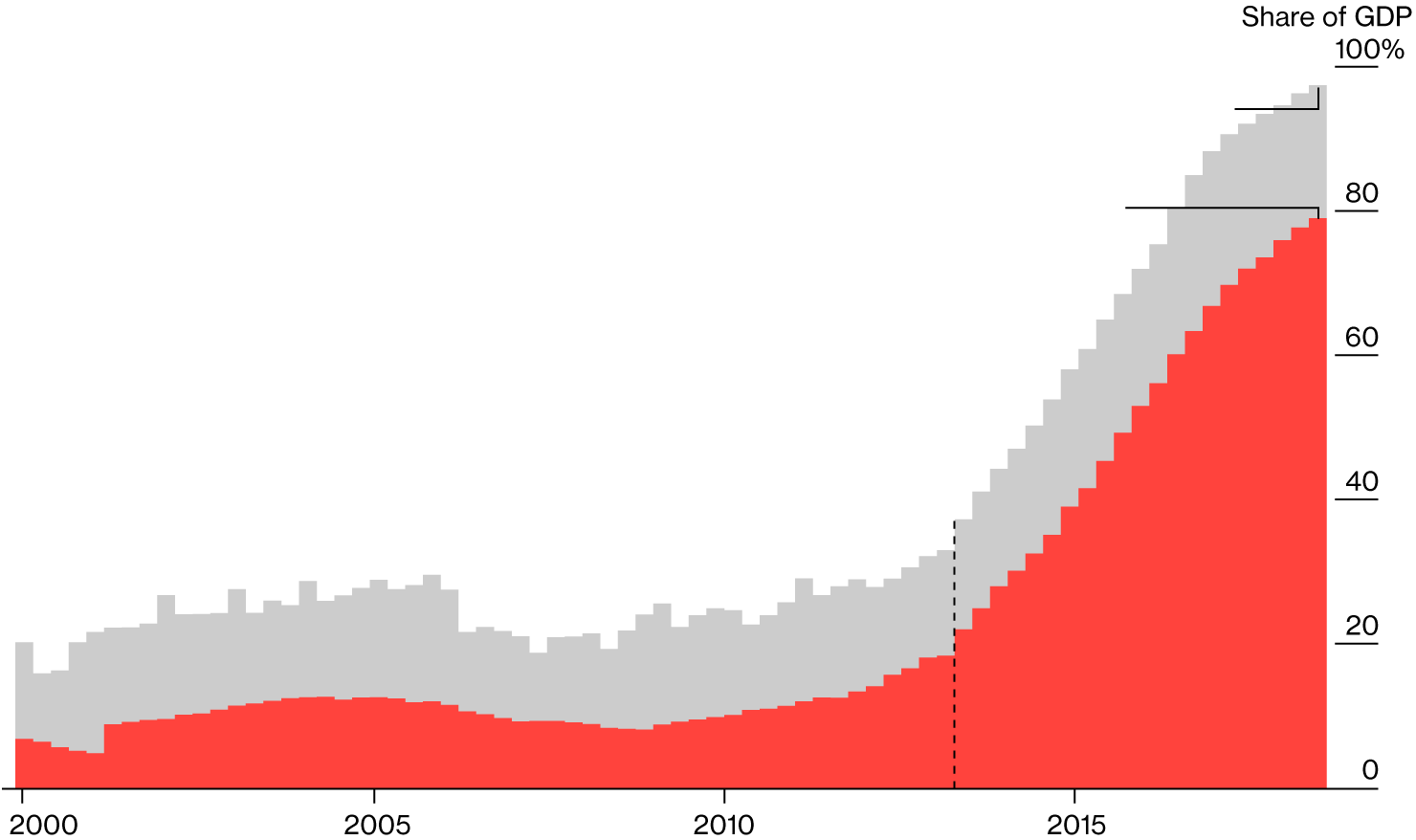

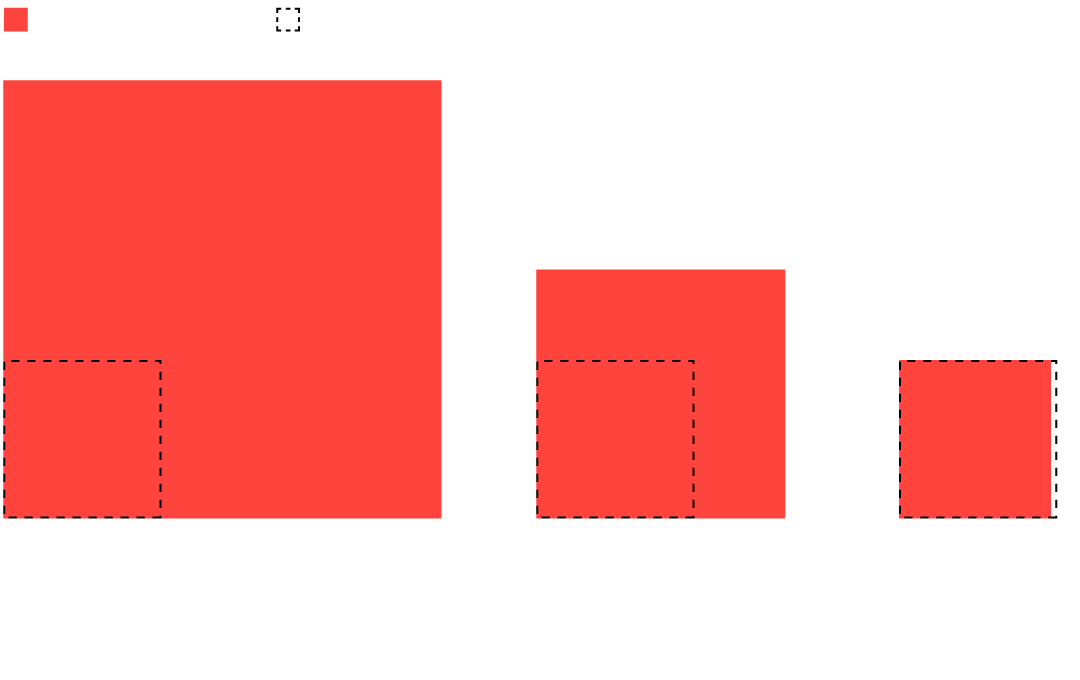

BOJ's Stimulus Has Dwarfed That of Its Global Peers

Bank of Japan

79%

0

2000

2018

European Central Bank

41%

0

2000

2018

U.S. Federal Reserve

21%

0

2000

2018

Bank of Japan

European Central Bank

U.S. Federal Reserve

79%

41%

21%

0

2000

2018

2000

2018

2000

2018

Bank of Japan

European Central Bank

U.S. Federal Reserve

79%

41%

21%

0

2000

2018

2000

2018

2000

2018

With Kuroda staying quiet on his longer-term plans, Bloomberg surveyed economists and market strategists for an exclusive analysis of what the end game could look like for the world’s most aggressive monetary stimulus of the modern era. There were some surprising results. For example, nearly half of analysts said there’s a moderate or high chance that a spike in interest rates during the BOJ’s exit makes it impossible for the government to manage its debt, threatening it with bankruptcy.

And if Kuroda is successful in reviving inflation to his desired 2 percent, the BOJ could lose tens or even hundreds of billions of dollars as interest rates rise and the value of its nearly $5 trillion in assets falls.

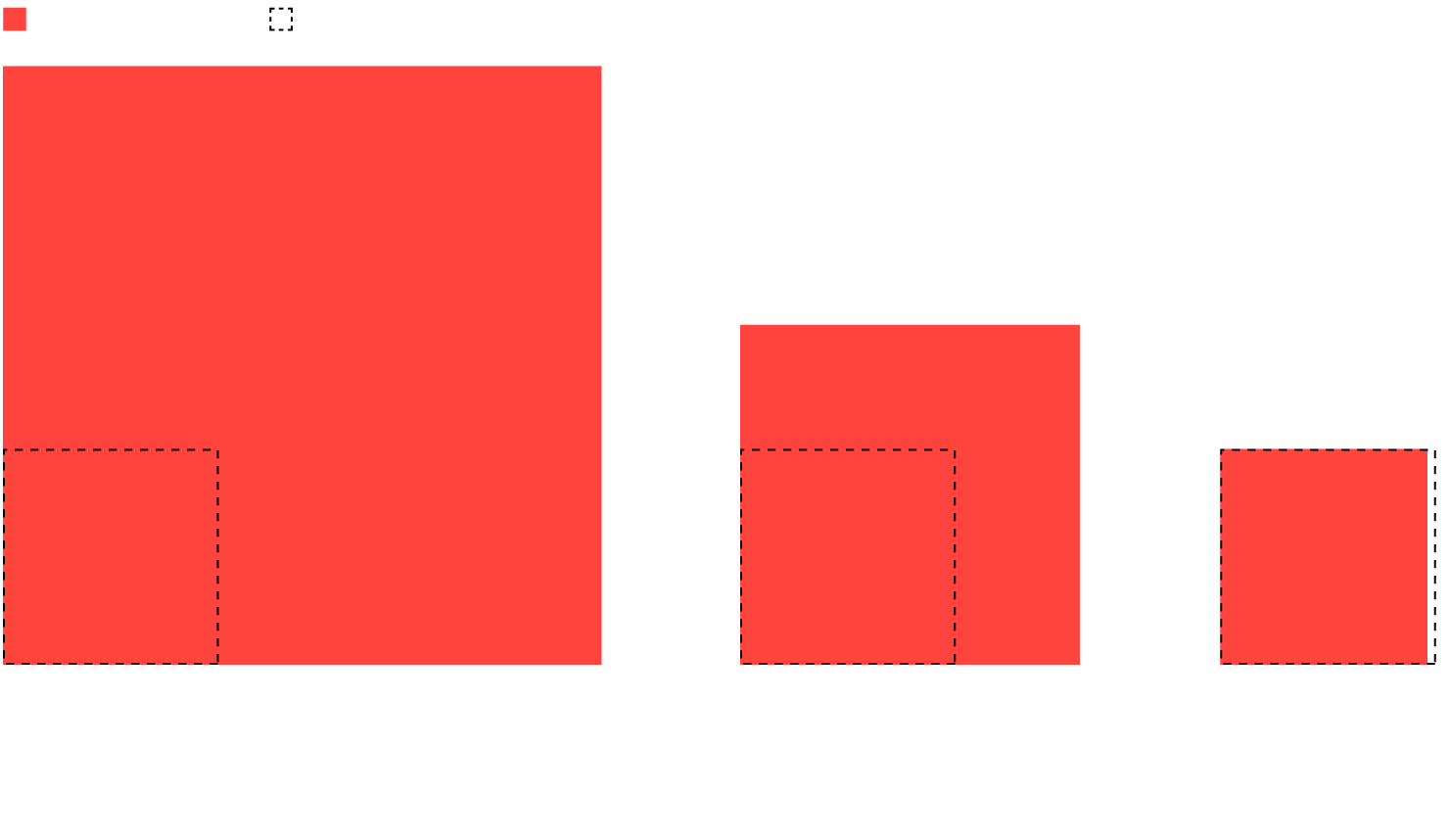

BOJ Finances at Risk

3%

Certain

25%

High

28%

Moderate

31%

Low

13%

No risk

13%

No risk

31%

Low

28%

Moderate

25%

High

3%

Certain

13%

No risk

31%

Low

28%

Moderate

25%

High

3%

Certain

Analysts cited the impact on commercial banks’ profitability as the biggest obstacle to the BOJ keeping its stimulus in place indefinitely. Years of rock-bottom interest rates have cut lending margins and deprived banks of low-risk gains from investing in Japanese government bonds (JGB), forcing them to take on more risk as they looked for other sources of profit.

While a little more risk was initially seen as a good thing, the BOJ never planned to keep its stimulus in place for so long. Its own gauge of lending attitudes among banks points to the highest tolerance of risk since the 1980s bubble era—and is at the edge of overheating.

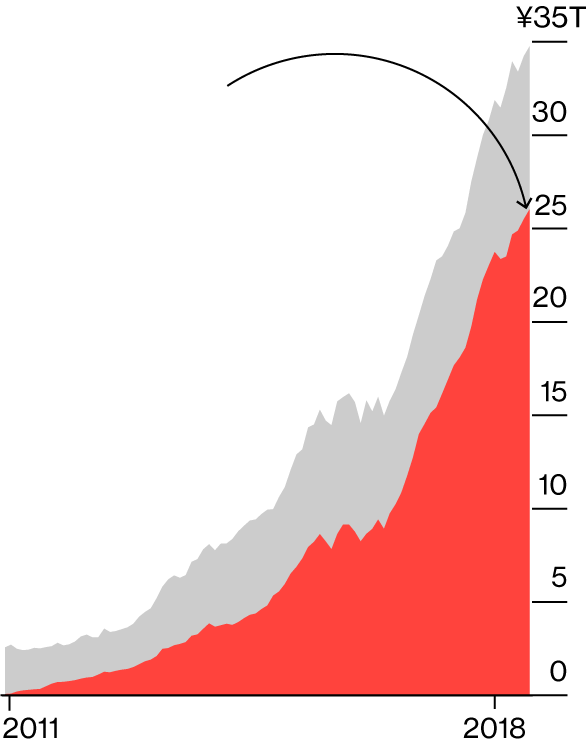

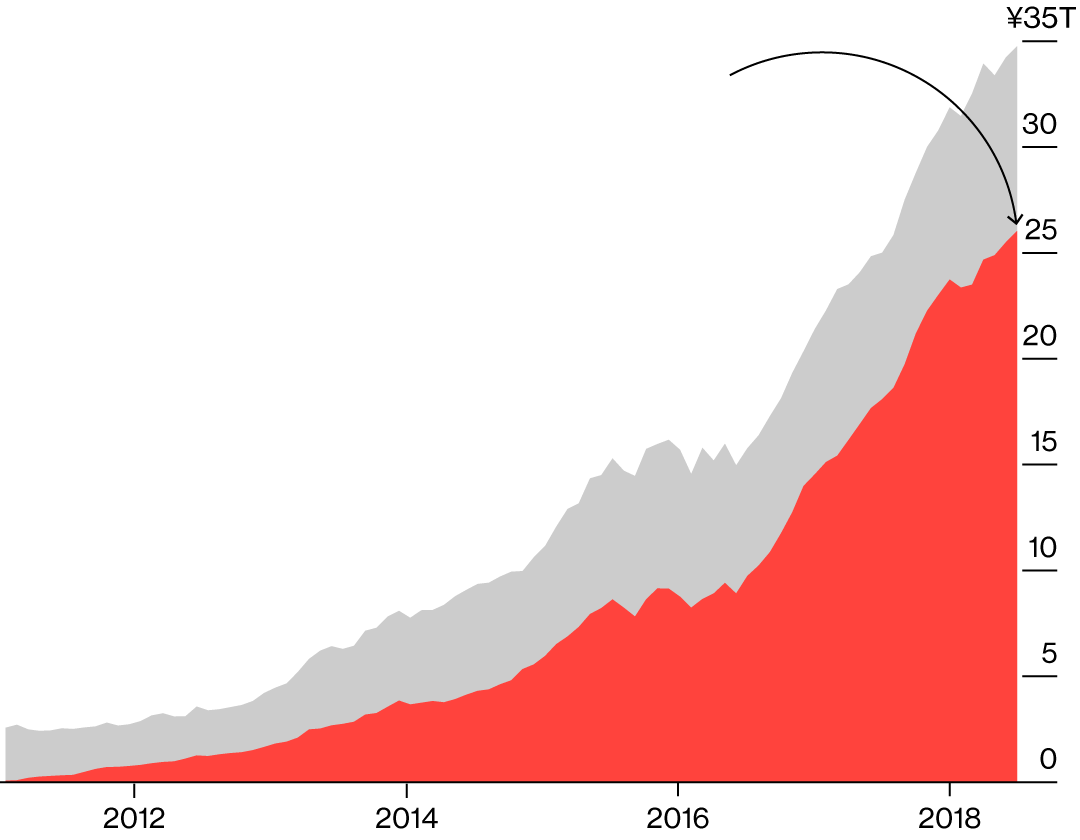

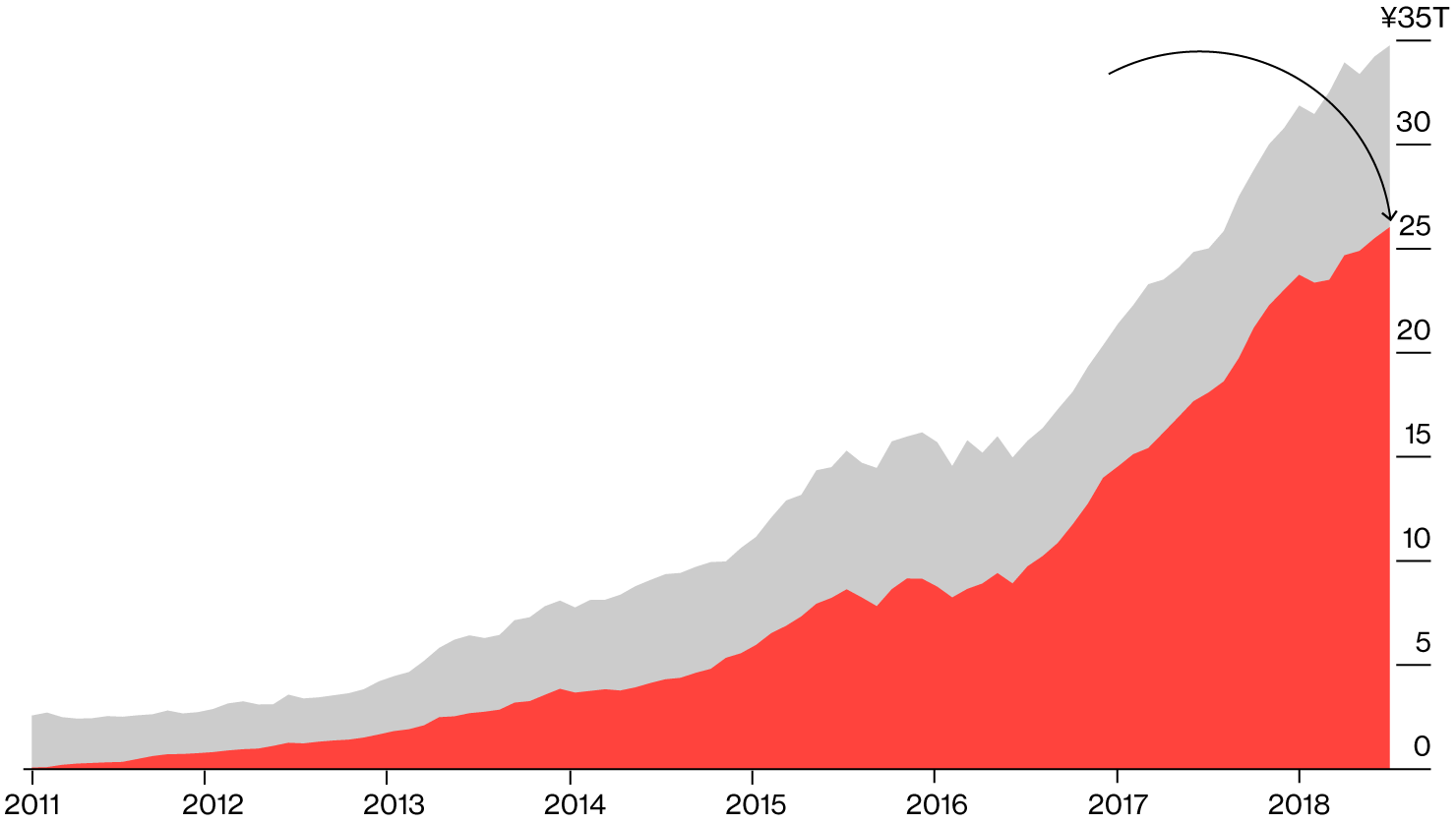

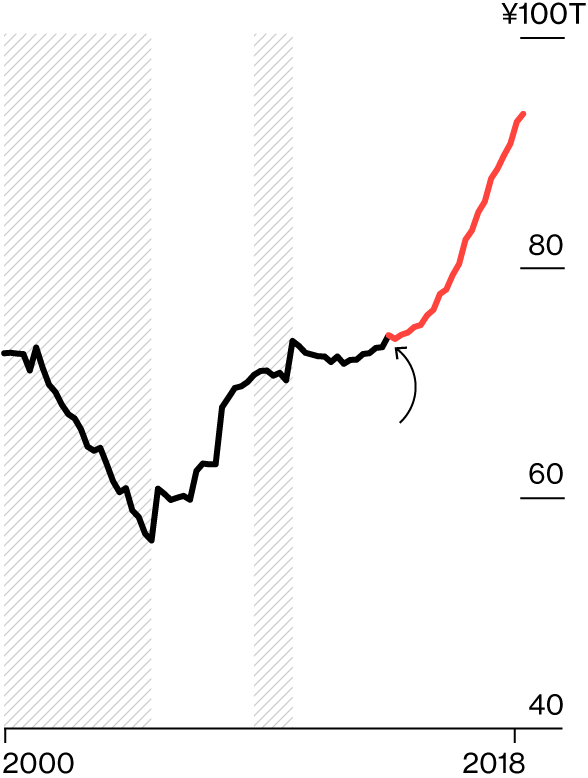

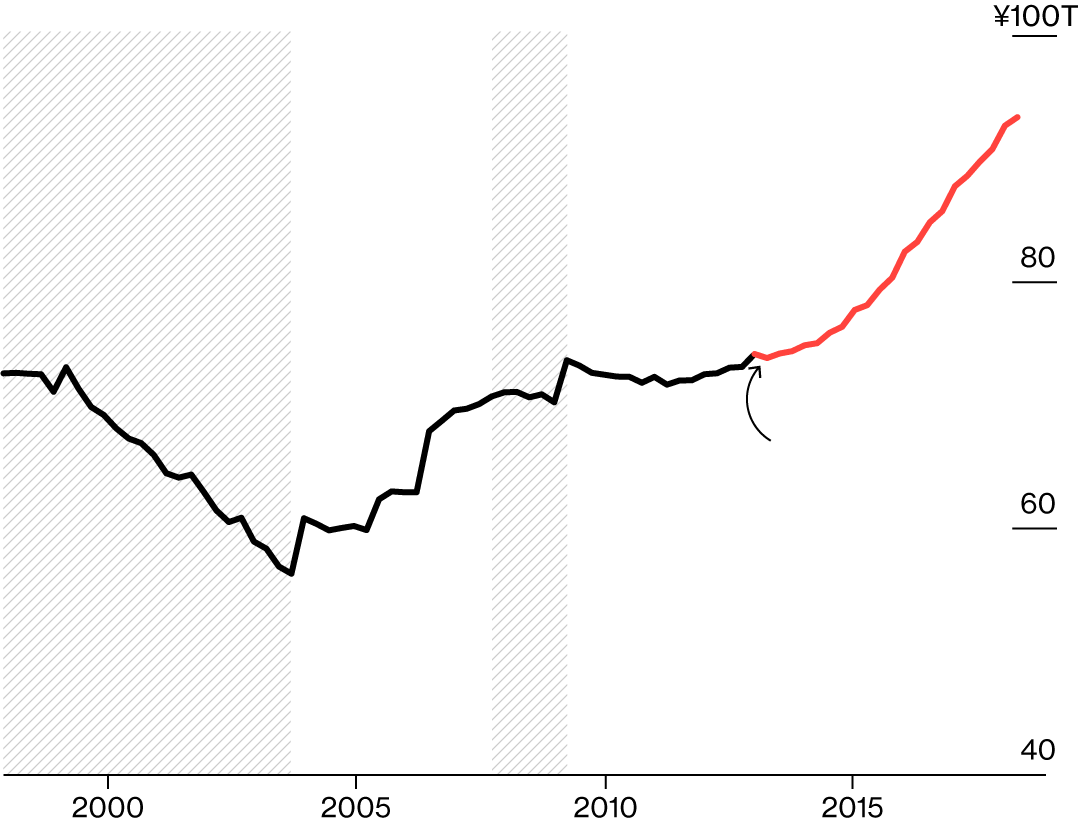

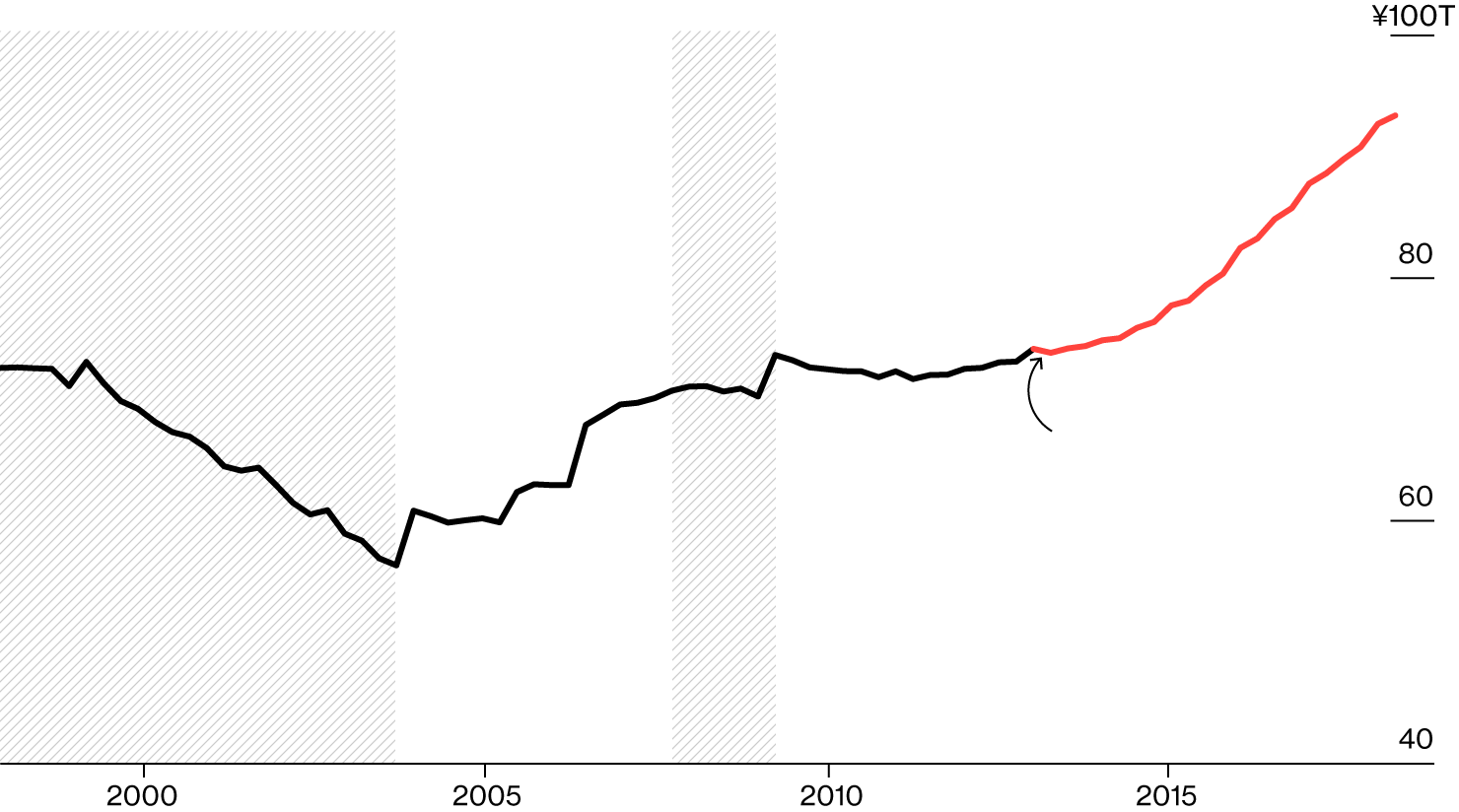

Mountain of Assets

Value of other assets:

¥107T

JGB holdings

¥450T

Kuroda’s stimulus started in April 2013

Value of other assets:

¥107T

JGB holdings

¥450T

Kuroda’s stimulus started in April 2013

Value of other assets:

¥107T

JGB holdings

¥450T

Kuroda’s stimulus started in April 2013

No. 2 on the list of reasons the BOJ can’t go on forever is the havoc it has caused in the market for government bonds. Its buying has dried up the supply of bonds, undermining the market’s critical function of pricing risk. And the more bonds the central bank buys, the bigger its potential losses when it exits. The BOJ is already tiptoeing away from asset purchases. Its annual bond-buying has slowed to nearly half its 80 trillion yen official guideline, even as that target remains unchanged in its policy statements.

The BOJ has also been snapping up equities—supporting bullish sentiment for now but creating a whole new set of long-term problems. The buying has been so extensive that it’s now among the biggest shareholders in a host of large companies—from Fast Retailing Co. to semiconductor firm Advantest Corp.—and owns three quarters of all shares in Japan’s exchange-traded funds.

Market Cornered

BOJ’s holdings account for 75 percent of the total ETF market

All others’

holdings

BOJ’s holdings account for 75 percent of the total ETF market

All others’

holdings

BOJ’s holdings account for 75 percent of the total ETF market

All others’

holdings

While the BOJ has indicated a willingness to slow its ETF purchases, selling its stock is another matter. Some 25 percent of analysts surveyed said there’s a high risk that selling would trigger a large decline in the market, and more than 40 percent said the BOJ would still be holding at least 25 percent of the nation’s ETF shares 20 years from now.

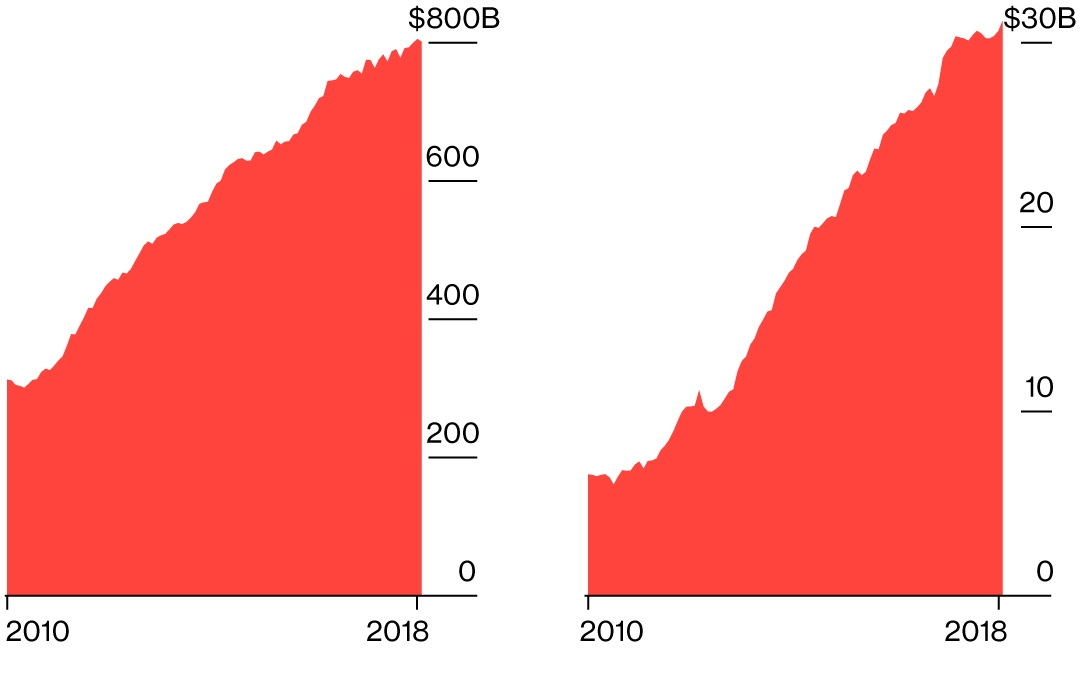

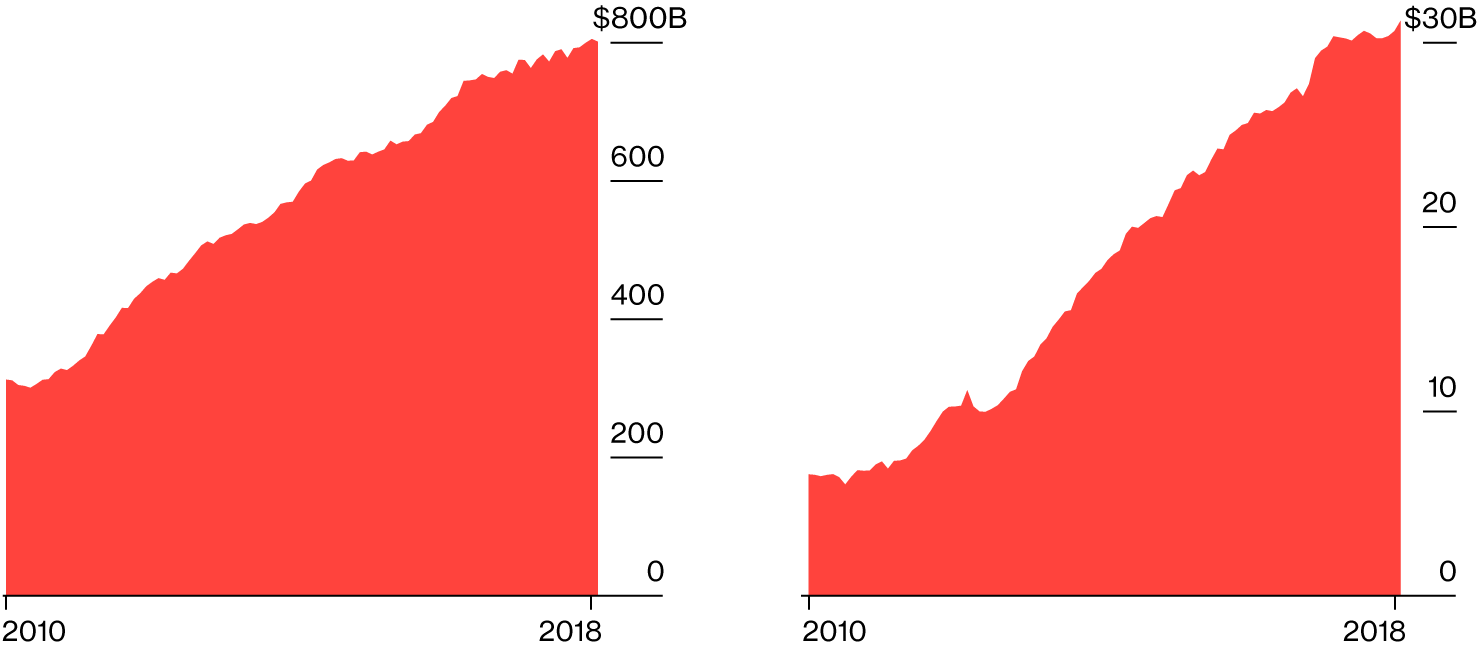

Faced with near-zero interest rates at home and soft demand for corporate loans, Japanese commercial banks have also continued to look abroad for profits. With overseas lending now accounting for about 30 percent of total loans at major banks, foreign currency-denominated assets have become a concern for regulators. They cite potential threats such as volatility in foreign-exchange markets, spikes in dollar-funding and hedging costs, and possible liquidity problems in times of market turmoil.

Outward Bound

Major banks

Regional banks

Major banks

Regional banks

Major banks

Regional banks

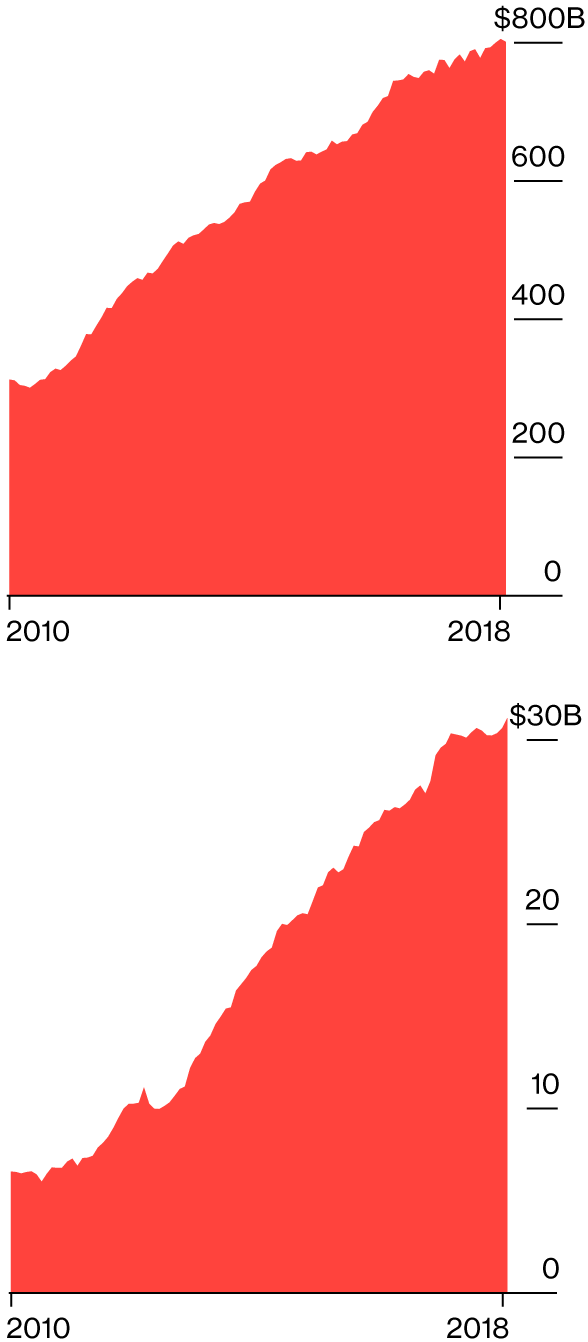

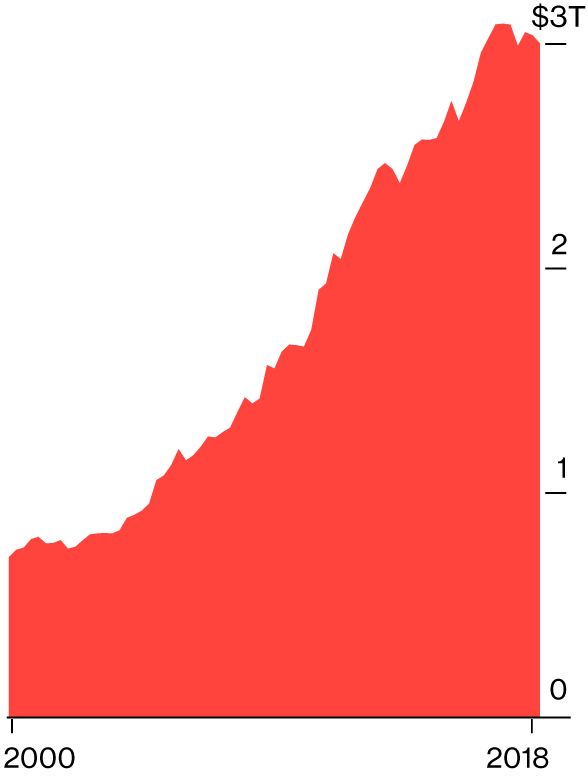

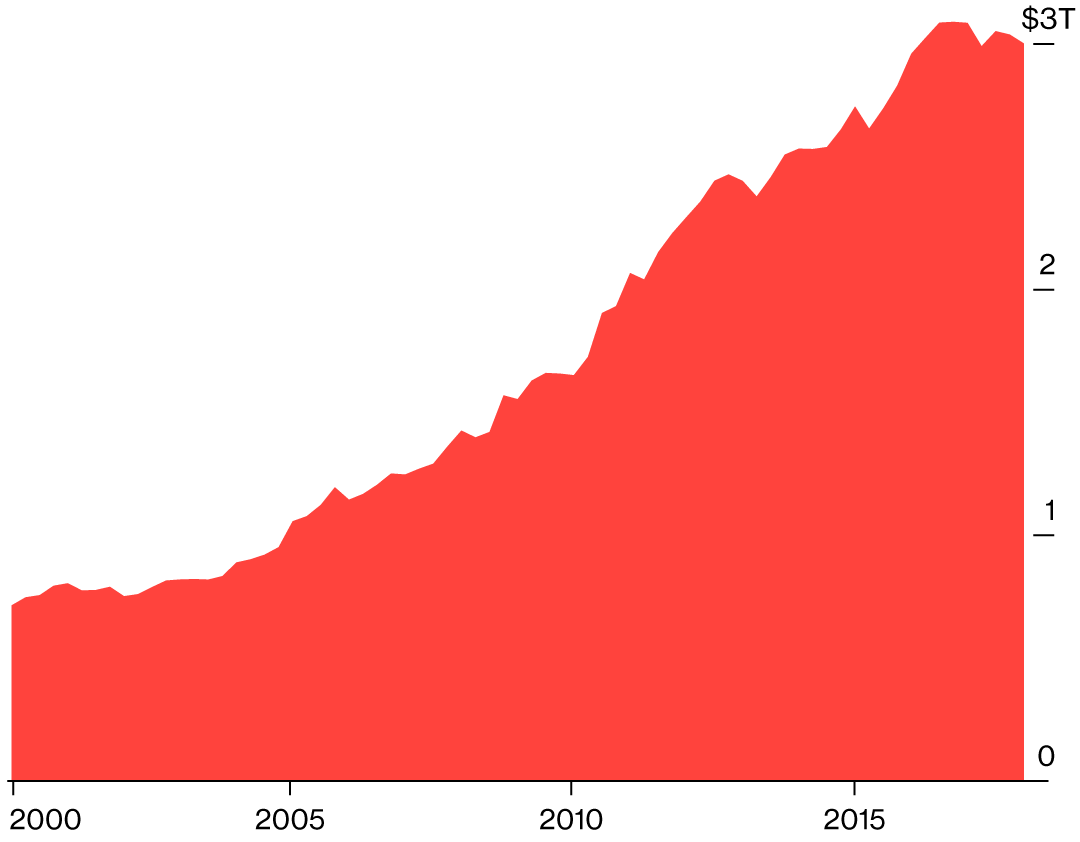

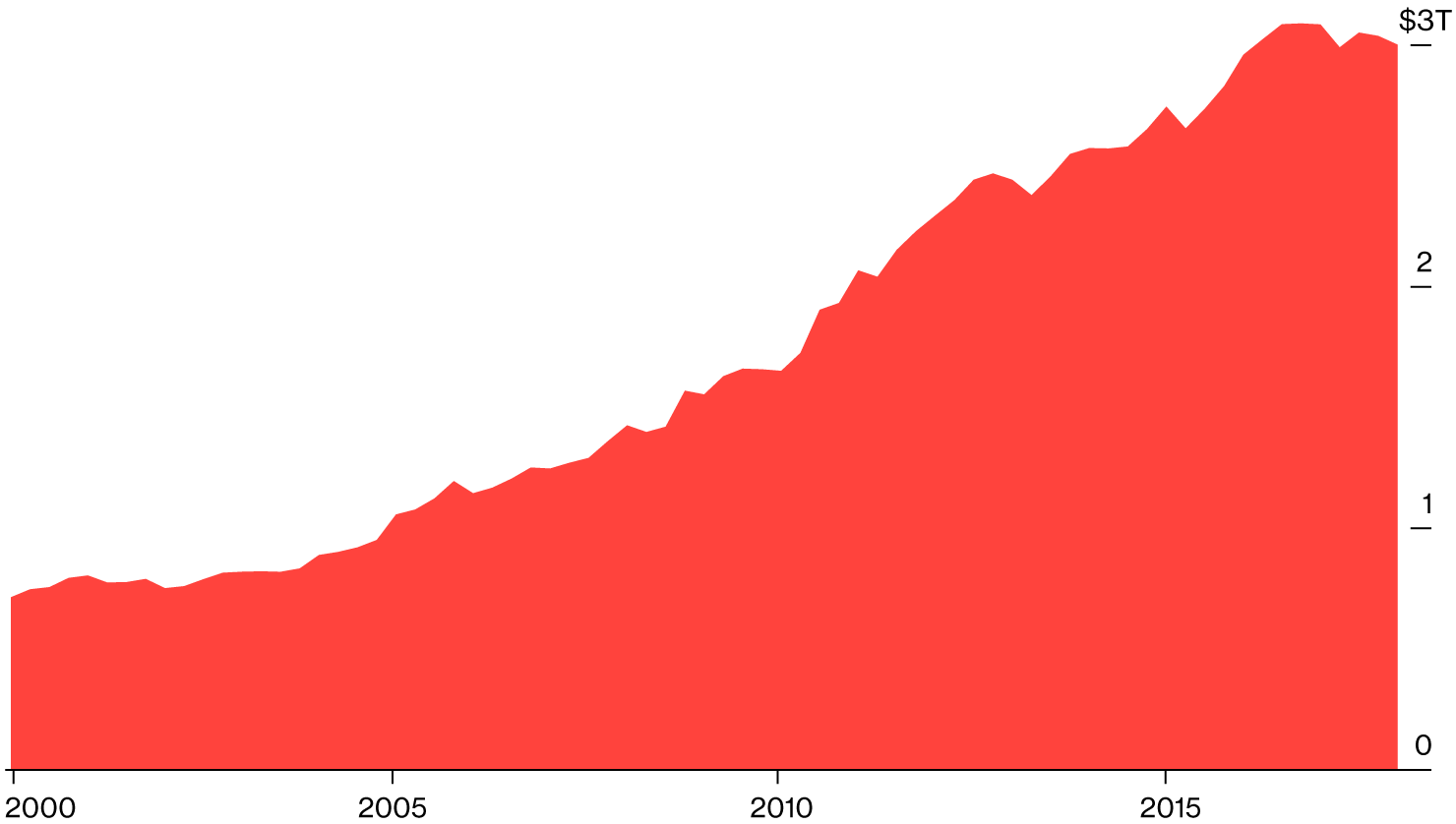

Japan’s institutional investors have been looking overseas as well. Holdings of foreign securities are up 28 percent over five years, to a record high of about $3 trillion. If the BOJ pushes interest rates higher, a lot of that money will start flowing back, adding unwelcome strength to the yen. That would undermine the BOJ’s efforts to stoke inflation and make Japanese exports more expensive on global markets. About three quarters of analysts said long-term Japanese rates of 1.5 percent or even 1 percent would trigger a significant reversal of those investments.

King Dollar

Lending for real estate has exceeded that to any other sector. It’s risen to record levels in absolute terms and as a share of the overall economy. The financial regulator is keeping a wary eye on property lending by regional banks, as well as the sustainability of some of their business models. Nobody is warning of a market collapse or crisis, and the BOJ even thinks some lenders have become more cautious lately. But real estate lending as a share of the economy is also approaching overheated territory, according to another central bank gauge.

Hot Property

Deflationary period in the aftermath of Japan’s asset bubble

Deflationary period in the aftermath of Japan’s asset bubble

Global

Recession

Global

Recession

Kuroda takes the helm of Bank of Japan

Deflationary period in the aftermath of Japan’s asset bubble

Deflationary period in the aftermath of Japan’s asset bubble

Global

Recession

Global

Recession

Kuroda takes the helm of Bank of Japan

Deflationary period in the aftermath of Japan’s asset bubble

Deflationary period in the aftermath of Japan’s asset bubble

Global

Recession

Global

Recession

Kuroda takes the helm of Bank of Japan

When the time comes, it could be costly for the BOJ to remove its stimulus. Some say it wouldn’t really matter if the BOJ suffered big losses because it can basically print money. But others say doing so would threaten the central bank’s credibility, invite political interference in its affairs and risk a collapse of the nation’s currency.

Price to Pay

Capital base

Estimated loss

¥59.5T

¥8.2T

Hiroshi Fujiki

Former BOJ official,

faculty at Chuo University

¥19T

Ikuko Fueda-Samikawa

& Tetsuaki Takano

Economists at Japan Center for Economic Research

¥7T

Takatoshi Ito

Professor

at Columbia

Capital base

Estimated loss

¥59.5T

¥19T

¥7T

¥8.2T

Hiroshi Fujiki

Former BOJ official,

faculty at Chuo University

Ikuko Fueda-Samikawa

& Tetsuaki Takano

Economists at Japan Center for Economic Research

Takatoshi Ito

Professor

at Columbia

Capital base

Estimated loss

¥59.5T

¥19T

¥7T

¥8.2T

Hiroshi Fujiki

Former BOJ official,

faculty at Chuo University

Takatoshi Ito

Professor

at Columbia

Ikuko Fueda-Samikawa

& Tetsuaki Takano

Economists at Japan Center for Economic Research

As if all of that weren’t enough, the 73-year-old BOJ governor must pull off the high-wire act of normalizing policy in an aging economy that’s as exposed as any to the ravages of a global trade war. It’s little wonder he’s loathe to even discuss how the greatest monetary experiment of them all will end.