Zombie Debt

Part II

No Cop on the Beat

Outside Chicago, a father of seven was too embarrassed to tell his family last Christmas that they might lose their home to foreclosure. A debt collector was demanding he pay almost $30,000 to settle a $10,000 second mortgage he said he hadn’t heard about in 15 years.

Another homeowner, near San Francisco, faced foreclosure this year over a $121,000 second mortgage — even though he’d received a tax document from his lender in 2009 showing the debt had been canceled.

And in suburban Washington, DC, a couple got a demand for more than $86,000 in back interest on a loan for which they hadn’t received any monthly statements in nearly a decade, despite laws that preclude any such interest charges during periods when regular statements weren’t sent.

In each of these cases and scores of others, borrowers went to court in last-ditch efforts to save their homes or challenge outsized interest payments on old second mortgages that could spell financial catastrophe. A nationwide review of lawsuits over these “zombie” mortgages showed that the vast majority of borrowers who sued ended up keeping their houses and beating back inflated bills after they were able to produce evidence that debt collectors violated consumer-protection laws.

Despite consumers’ piecemeal victories, debt collectors continue to extract huge paydays on long-forgotten loans from homeowners, many of whom don’t have the means or wherewithal to get legal help. Bloomberg News identified more than two dozen firms that took over second loans belonging to at least 12,000 homeowners. These “zombie debt collectors” were among the most active in pursuing old second mortgages and faced lawsuits from borrowers who contested their efforts to collect. Hundreds of thousands more borrowers remain exposed on more than $32 billion of the old loans.

A major reason why: There’s no federal cop on the beat because President Donald Trump’s administration gutted the agency tasked with enforcing consumer-protection laws.

Zombie Debt Collectors Revived Old Loans Nationwide

Loan assignments to zombie debt collectors

10

100

Insufficient data

Source: Bloomberg analysis of public property records aggregated by Attom Data Solutions (Download the summary data.)

Note: Data for 2015-2025. An assignment of a mortgage is an official public record that transfers a mortgage loan to a new creditor. Assignments often represent just a fraction of a debt collector’s portfolio because not all ownership changes are recorded publicly. To account for incomplete data coverage in some regions, the analysis is limited to congressional districts where Bloomberg could get records on at least 1,000 second mortgage originations between 2002 and 2008 and at least 10 assignments since 2015.

A handful of states have adopted new statutes to address unlawful zombie debt collections in recent years, and at least one state has sued a firm that made a business of collecting the old loans. But in most of the US, borrowers have been left on their own to defend themselves when debt collectors demand their money or their homes.

“There is no way the private bar or the states can identify and address the scope of the zombie second mortgage problem,” said Diane Thompson, deputy director of the National Consumer Law Center.

Yet, as Bloomberg reported earlier this month, a planned federal enforcement effort has stalled out under Trump.

Investigators from the Consumer Financial Protection Bureau had been building cases earlier this year against at least three companies involved in zombie mortgage collections, according to two people with direct knowledge of the effort who asked not to be identified discussing investigations.

The Trump administration functionally halted that work in February when the CFPB’s acting director Russell Vought ordered the cessation of supervision and examination activity and later sought to fire nearly all of the agency’s staff. Congress then slashed CFPB’s funding nearly in half as part of the president’s spending bill in July.

A White House spokesperson who handles inquiries for the CFPB told Bloomberg in September that it’s “completely false to claim work on these cases has been ‘abandoned’” but wouldn’t elaborate.

Earlier this month, however, Vought, who is also the director of the US Office of Management and Budget, told The Charlie Kirk Show that he plans to shut down the consumer-protection agency “within the next two to three months.” Vought said CFPB had failed to protect consumers and instead had been weaponized to harm small lenders and financial institutions. The White House didn’t respond to a request for comment about Vought’s remarks.

Shutting the agency could further weaken, if not eliminate, enforcement of key laws meant to protect consumers when dealing with their mortgage companies. In the aftermath of the 2008 financial crisis, Congress created the CFPB and tasked it with enforcing those laws, replacing a patchwork of agencies that the crisis had shown to be ineffective.

“Americans are being tricked and trapped by zombie mortgages,” said Senator Elizabeth Warren, the Massachusetts Democrat who’s widely acknowledged as the CFPB’s intellectual architect. “The CFPB should be protecting Americans from these scams, but instead Donald Trump and his administration are abandoning American homeowners.”

The CFPB was investigating zombie debt collectors before the Trump administration gutted the agency. Photographer: Al Drago/Bloomberg

Economist Douglas Holtz-Eakin, who was an adviser to Republican Senator John McCain’s 2008 presidential campaign and a member of the Financial Crisis Inquiry Commission, said zombie mortgage cases present a clear need for enforcement. Although he didn’t agree with the structure of the CFPB when it was created, he said that Congress tasked it with upholding the laws that matter most in zombie mortgage cases.

“There should be someone on this watch,” said Holtz-Eakin, who is now president of the American Action Forum, a center-right think tank. “You have to enforce these abusive-practice laws and disclosure laws vigorously to make sure that people will always think the laws are on the side of fairness.”

In response to court challenges, debt collectors have said that they follow the law, that the debts they’re seeking to collect remain valid and that they have a right to collect. Last month, mortgage-industry trade groups and several anonymous lenders filed a federal lawsuit to challenge a new California law that’s meant to protect homeowners. They argued that the abuses the legislation sought to address are outliers and the new law is so burdensome it will stifle home lending.

The Association of Credit and Collection Professionals, which sets ethical standards for third-party collection agencies, law firms and asset-buying companies, said few of its members collected zombie mortgages. But, to the extent they do, “they would typically have a robust compliance program that accounts for both state and federal laws and regulations.”

David Gordon, one of the managing partners of ARC, a company that Bloomberg featured in a story about zombie mortgages earlier this month, said it’s important for creditors to be able to collect on defaulted loans and that such rights ensure a functioning mortgage market.

“If you have a problem with this, talk to Congress,” he said.

Today’s zombie second mortgages stem from the years before the 2008 financial crisis, when a US housing bubble was inflating. At the time, lenders eagerly gave homebuyers two loans — a first mortgage to cover the majority of the purchase price and a second to reduce or eliminate the need for a cash downpayment. At the peak of the subprime housing bubble, roughly a quarter of all homebuyers took out these smaller “piggyback” loans. Others got home-equity lines of credit, tapping into rising property values. After housing prices crashed, second mortgages became practically uncollectable, and lenders modified them, canceled them or just stopped trying to get borrowers to pay them back.

Years later, as home prices recovered enough to make foreclosures a credible threat again, debt collectors who’d bought up the old loans — usually for pennies on the dollar — began making demands for repayment along with years of back interest. These included both amateur investors and more established firms, with portfolios that include more than just zombie mortgages.

While it’s impossible to determine how many old second mortgages are now controlled by zombie debt collectors, there are plenty of the loans out there. Using public property records aggregated by Attom Data Solutions, Bloomberg examined more than 5.5 million piggyback mortgages issued between 2002 and 2008. After removing loans that were likely refinanced or paid off, an estimated 600,000 of these old second mortgages remain.

These old loans typically only resurface publicly after debt collectors disclose that they’ve acquired them by filing documents called assignments with county recorders. Bloomberg examined records related to more than 120 lenders that had the highest number of second-mortgage assignments nationwide since the beginning of 2015. Among this group, zombie debt collectors were three times more likely, on average, to initiate foreclosures than other creditors were.

Zombie Debt Collectors Foreclose More Often

Zombie debt collectors

Foreclosure rate

Banks and other creditors

Source: Bloomberg analysis of public property records aggregated by Attom Data Solutions

Note: Foreclosure rate between 2015-2025. The chart excludes creditors with fewer than 50 assignments. See methodology for details.

Such aggressive tactics can overwhelm borrowers; the fear of losing their homes has driven thousands to pay up, even if it wasn’t clear they owed everything the collectors claimed. According to industry insiders and former regulators, borrowers who kept their first mortgages current are the most at risk. That’s because they’ve built up equity in their homes and, since they have more to lose, they’re considered more likely to cut a deal that’s favorable to debt collectors. Academic research, drawing on data provided by a hedge fund, found that borrowers who get caught up on their first mortgage were more likely to pay up on the second.

“These are not people who went off and got some great deal and are mooching off the public,” said the NCLC’s Thompson, who was a former top official at the CFPB during the Biden administration. She declined to speak about confidential regulatory efforts. “The only reason the debt buyers are coming after them now is because they’ve been able to stay current on their first mortgage.”

Raul Esparza, a foreman carpenter who lives outside Chicago, is the kind of person Thompson is describing. During the downturn, he fell behind on the two mortgages he took out to purchase the modest home where he and his wife raised their seven kids. In 2009, he modified his first loan and has kept up with payment since.

After 15 years of not hearing anything about the second loan, he said he got a demand letter in September 2024 from a law firm, attaching a billing statement from Franklin Credit Management Corp. that said he owed more than $29,000 in back interest and principal on the old $10,000 debt. He couldn’t understand why a company that thought it was owed that kind of money would wait a decade and a half to collect.

“If I don’t pay water, gas, if I don’t pay my car, they’ll be here in three, four months,” he said.

Sitting at his dining room table in May, he choked up describing the shame he felt when he realized he might lose the house he’d spent years fixing up himself and that he hopes to pass onto his kids. “I’m responsible for it,” Esparza said. “It’s their childhood home.”

Raul Esparza and his wife, Gabriela, outside of their home in Midlothian, Illinois, where they have lived for more than two decades. Photographer: Kayana Szymczak/Bloomberg

Earlier this year, his son helped him hire a lawyer to fight the foreclosure, and it was dismissed in April. Although the judge in the case recently agreed to reconsider that decision, he also ruled that too much time had passed under Illinois law to collect at least some of the money the companies asserted Esparza owed. As the process has dragged out, the case has cost Esparza’s son thousands of dollars. Esparza has filed a separate lawsuit against the debt collectors seeking damages; it is ongoing.

Franklin Credit, which settled with Massachusetts regulators last year over allegations it violated state consumer-protection laws in trying to collect old second mortgages, didn’t respond to a request for comment. In court filings, the Jersey City, New Jersey-based company denied any wrongdoing in both the Massachusetts case as well as Esparza’s.

Jose Rivas, a flooring contractor in Hayward, California, said he was also current on his first mortgage when a debt collector came to demand money related to a zombie second mortgage. Like Esparza, he found that the court system offered him imperfect protection.

In March, a company named Dyck-O’Neal foreclosed on his house, saying he was in default on a $121,000 second loan he had taken out in 2005 from New Century Mortgage, a now-defunct company that was once one of the nation’s largest subprime lenders.

Rivas told Bloomberg he hadn’t received any statements for the second mortgage since 2009, when he got a tax document called a 1099-C, stating that the debt had been canceled. Then, one day last December, nearly 16 years later, he came home from a trip to El Salvador to find a notice of trustee sale tacked to his door.

“I thought it had to be a scam,” he said.

He knew that his first mortgage was current, so he didn’t do anything about the notice. A few months later, he was told that his home had been sold at a foreclosure auction — and that his family had to move out. Since then, he’s racked up tens of thousands of dollars in legal bills to stay in the house, where he lives with his wife and children.

Jose Rivas, his wife and daughter in their California home. Photographer: Rachel Bujalski/Bloomberg

Dyck-O’Neal didn’t respond to repeated requests for comment. The Dallas-based firm is a major player collecting zombie mortgages, according to Bloomberg’s analysis of property records. At least six homeowners have sued the company, alleging it violated a federal debt-collection law and regulations requiring regular statements.

Last month, Dyck-O’Neal said in a legal filing that Rivas “did nothing to tender or cure the arrearages” on his mortgage before the foreclosure auction this year.

Rivas reached a settlement in September to repurchase his house from a company that bought it at auction, but he’s still pursuing claims against Dyck-O’Neal for damages, according to his attorney, Sarah Shapero.

Rivas said the expense has pushed back his dream of paying off his mortgage and retiring. “I only had like 10 more years,” he said. “I was trying to do everything right. And then this happens.”

Before the CFPB lost most of its staffing, its investigators believed they had enough evidence to file civil lawsuits against three firms involved in zombie debt collections, according to two people with direct knowledge of the effort. In each of these cases, the agency was targeting a specific type of business: mortgage servicers.

Servicers are hired by debt owners to handle the day-to-day management of their loans, such as generating statements and collecting payments. When mortgages are in default, servicers often are the ones sending demand letters and providing borrowers with their options to pay back any arrears.

The consumer-protection agency’s officials thought that focusing on servicers — instead of the companies that bought zombie mortgages — would be an effective deterrent to unlawful collections. If these servicers thought regulators were scrutinizing their work on these old debts, fewer of them would take on the business, making it more difficult and costly for debt buyers to pursue collections, the people said.

Earlier this year, the CFPB was investigating Veripro Solutions, Specialized Loan Servicing and FCI Lender Services — all of which had done loan servicing for zombie debt owners. Whether or not the cases would lead to enforcement actions remained to be seen. The people said the agency was focused on alleged violations of the federal Fair Debt Collection Practices Act, which bars debt collectors from demanding amounts they know to be incorrect and from seeking repayment of any loan that has passed its statute of limitations. (Such limits range from a few years to a decade or more after a debt becomes due in full, depending on the state and type of loan.)

While investigators were gathering evidence, Veripro announced it would shutter. Its parent, Mr. Cooper Group Inc. was acquired by mortgage giant Rocket Cos. this month, and neither company responded to repeated requests for comment.

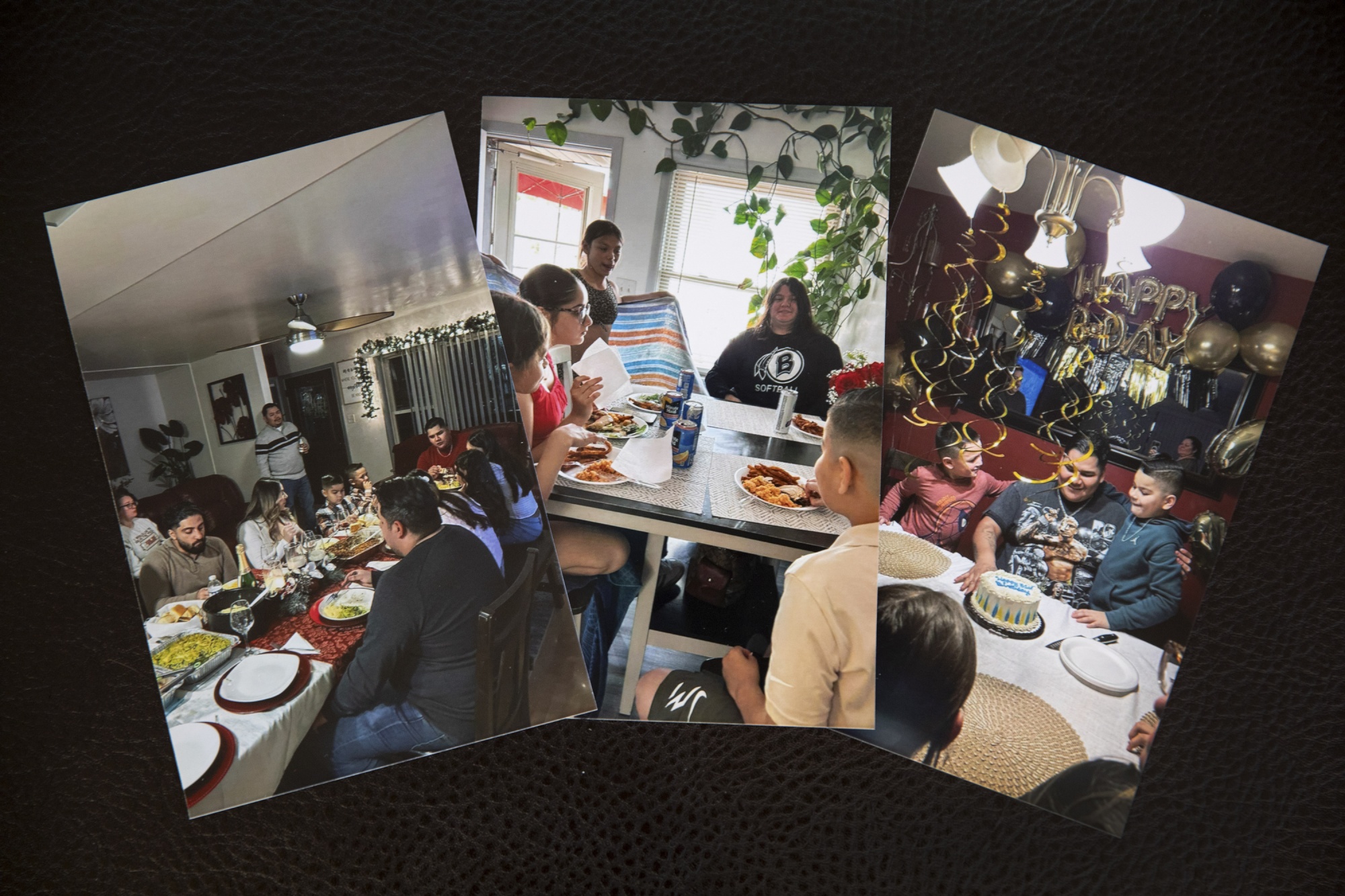

Photos of various family gatherings and celebrations in Raul Esparza’s home, which he hopes to pass on to his children. Photographer: Kayana Szymczak/Bloomberg

SLS merged with mortgage lender and servicer Newrez. A spokesperson said the company couldn’t comment on “potential or existing confidential supervisory matters.” He added that the business has procedures in place to comply with rules related to second mortgages.

FCI also didn’t respond to requests for comment. CFPB investigators found that the servicer did a lot of business for small investors who’d purchased zombie debts, according to people familiar with the agency’s work. These owners of the debt were particularly troublesome to officials, because they often lacked the expertise or sophistication required to follow the law, the people said.

The California-based company says it has more than 8,200 clients and says online that its platform works as well for Wall Street firms as it does for mom-and-pop operations. Bloomberg reviewed 13 private lawsuits against the company. In those cases, borrowers alleged some combination of receiving inaccurate payment demands, no regular statements or untimely responses to requests for basic information about their loans. FCI denied the allegations in court filings and settled most of the cases.

One FCI client was a business run by active and retired Colorado firefighters. That company, Devgru Financial LLC, foreclosed on homeowners in New York, Arizona and Georgia, records show.

One of Devgru’s owners Herb Dorn, a retired firefighter and mountain rescuer, said it had fewer than 100 old second loans on its books. The firm pulled back from distressed debt collection because it was too hard to compete with larger companies and deal with compliance issues, Dorn said. Massachusetts officials said the firm was operating as an unlicensed debt collector and sanctioned the company in 2021.

As Danielle and Roy Brown would learn, even bigger, more sophisticated debt buyers have been accused of failing to follow the law when collecting zombie loans.

US District Judge Leonie Brinkema was working through a busy docket last June when she dispensed some blunt advice to two corporate defense lawyers standing in front of her:

“You ought to settle this case.”

The attorneys were trying to get the judge to dismiss a class-action lawsuit, alleging a group of zombie debt collectors had illegally charged homeowners back interest on old second mortgages.

Judge Brinkema, a four-decade veteran of the federal bench, wasn’t having it. “These ghost mortgages are really nasty things,” she said before ruling the class-action could go forward.

The judge’s decision was a small victory for Kristi Kelly, a public interest lawyer in Fairfax, Virginia, who has become a specialist in fighting zombie debt collectors. “It’s all about greed,” she said. “They don’t care about the homeowners who have fought to stay in these homes. It’s, to me, one of the most offensive things I’ve seen in my legal career.”

Kristi Kelly, a public interest lawyer who filed a lawsuit on behalf of Danielle and Roy Brown, in her office in Fairfax, Virginia. Photographer: Alyssa Schukar/Bloomberg

In another case, she found a debt collector demanded that a Virginia man pay more than $193,000 to settle a $79,000 second mortgage or risk losing the home he shared with his son and grandchildren. The firm had purchased the loan for just 67 cents.

Kelly’s firm filed the class-action suit on behalf of Danielle and Roy Brown, a couple in Loudoun County, Virginia, and more than a thousand other borrowers across the country. To pursue the case, she had to solve a few mysteries that the homeowners, on their own, simply couldn’t.

When the Browns bought their home in 2001, it was one of the first built on their block in suburban Washington, DC. They raised three daughters there over the following two decades as more houses sprang up in the neighborhood. Then, last summer, a debt buyer initiated foreclosure on an $89,000 loan they thought had been erased nearly 10 years earlier.

They’d taken out the second loan in 2005 to pay down debt and make home renovations. Then the couple ran into financial difficulties stemming from the financial crisis after Roy lost his job. In 2012, they were able to modify their first mortgage — and, they assumed, their second.

Like many borrowers who modified loans at the time, the Browns believed their new loan included both debts. After all, it was with the same company, and it was larger than the first mortgage because it reflected missed payments. Moreover, the Browns said they stopped receiving statements on their second loan in 2013, giving them the impression that both loans had been rolled into one.

But in June 2022, they suddenly started receiving statements on the old second mortgage that reflected balances vastly larger than the original principal. By that December, they got a demand to pay $182,237.21, including more than $86,000 in back interest. Their long-forgotten second mortgage had been bought in November 2021 by an entity called Star214 LLC. They’d never heard of the company and were confused when the bills started arriving.

Kelly eventually figured out that Star214 was one of more than two dozen entities linked to Connecticut-based Shelving Rock. That firm’s longtime chief executive officer, Stephen Lamando, was a Goldman Sachs alum with a background in mortgage markets. Lamando died in 2023, but his name appears on corporate records for several limited liability companies that, in addition to the ones Kelly found in her lawsuit, collectively had one of the highest foreclosure rates among zombie debt collectors in Bloomberg’s analysis.

It Can Be Hard to Tell Who Owns Zombie Mortgages

Source: Bloomberg News review of legal and corporate filings

Depositions taken in the case show that Shelving Rock was working hand-in-glove with a Colorado-based servicer called Statebridge. Neither firm, nor their attorneys, responded to requests for comment. Both companies denied allegations of wrongdoing in court filings.

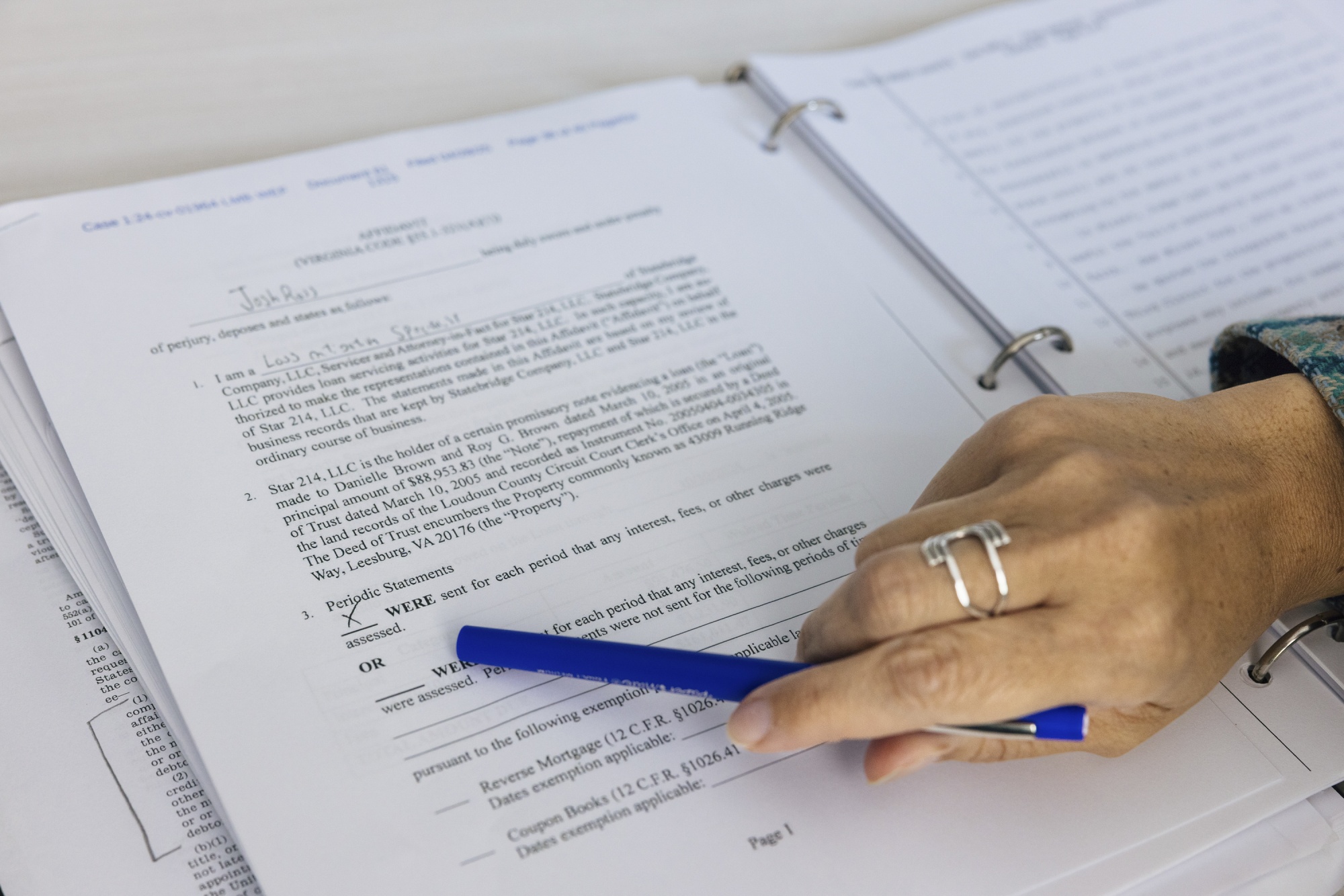

Thanks in part to their lawyer, the Browns had a new way to fight the claims from Shelving Rock and Statebridge. In 2024, Kelly had pushed Virginia lawmakers to pass legislation requiring debt collectors to attest that monthly statements had been sent to detail every period for which they were seeking back interest. That requirement forces debt collectors to verify that the amounts they’re demanding from borrowers are accurate, and it makes it easier for homeowners to fight unlawful demands for back interest in court.

After filing the case, Kelly and a colleague found a signed affidavit from a Statebridge employee saying “periodic statements were sent for each period that any interest, fees, or other charges were assessed.” Yet, during a deposition, the same employee testified no statements had been sent between 2013 and 2022 — meaning the Browns were charged far too much, according to Kelly.

Kristi Kelly shares an affidavit from the case at her office in Fairfax, Virginia. Photographer: Alyssa Schukar/Bloomberg

“No statements sent on the Browns’ loan from 2013 until it was boarded at Statebridge in 2022; correct?” Kelly asked.

“Yes,” he replied.

In September, Statebridge took Judge Brinkema’s advice and reached a preliminary settlement in the class action.

The proposed agreement, which is subject to a final approval hearing in January, means the Browns would have their entire debt erased. Other borrowers may see reductions of tens of thousands of dollars as well as damages. Any foreclosures involving members of the class action would be paused until at least mid-February, allowing homeowners time to understand what, if anything, they actually owe.

Danielle Brown feels that some justice is being done in her case and for others who have suffered similarly. But she’s under no illusion that one class action is enough to address the larger problem.

“This is a bigger issue than one state,” she said. “This needs to be solved federally.”