Zombie Debt

Part III

Rise of the ‘Zombie’ Loans

Shawn Murphy was stationed in South Korea with the US Army Corps of Engineers in late 2022 when his sister told him she had cervical cancer. He immediately flew home to Los Angeles to help her and eventually began thinking of ways to pitch in on the medical bills.

An obvious source of money was Murphy’s duplex in Hollywood. It had appreciated significantly since he’d purchased it in 2003, and he figured he could pull out some cash by refinancing.

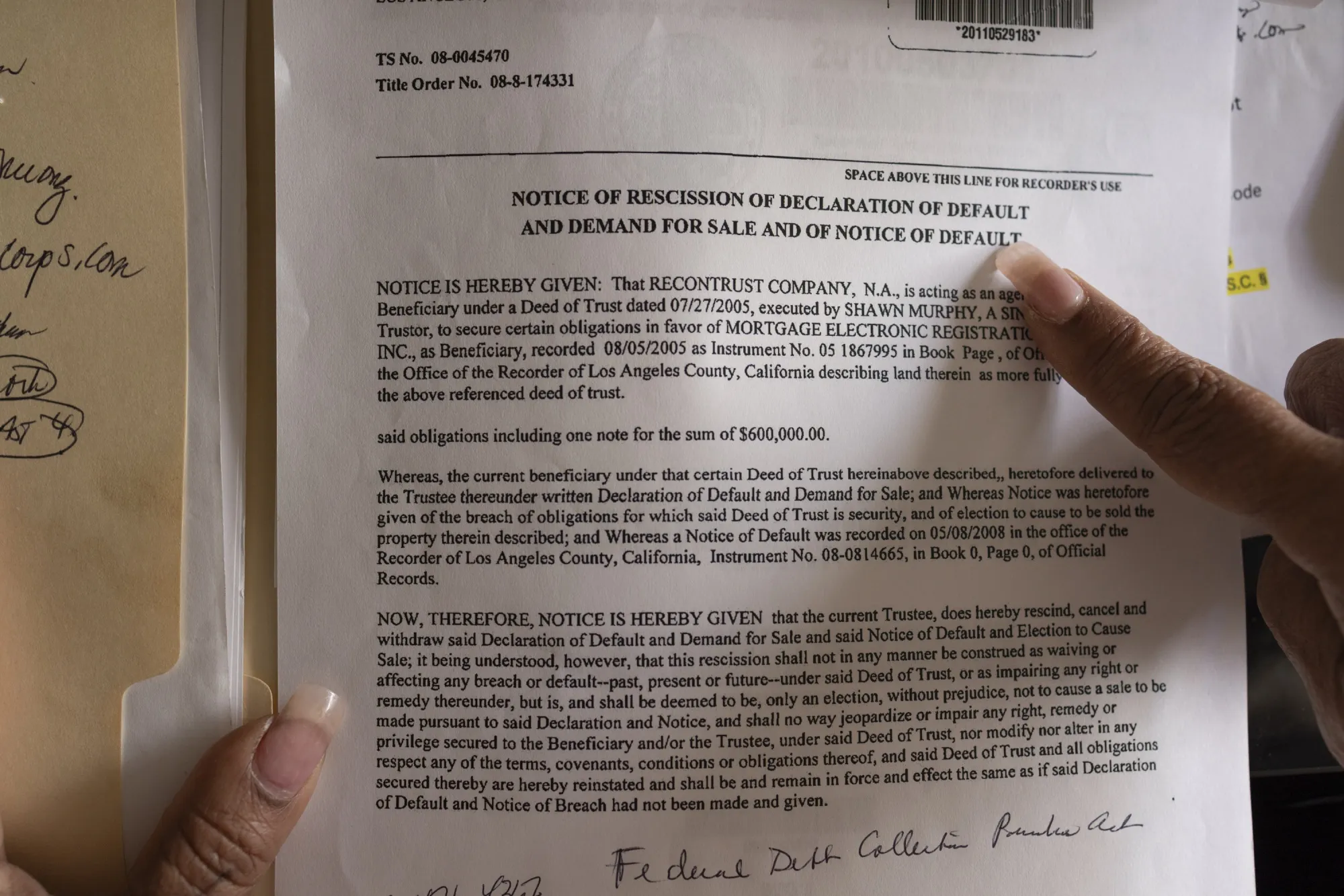

In looking into a loan, however, he was shocked to find a lien on his house for a second mortgage he’d taken out nearly 20 years earlier. He said he hadn’t heard about the debt since his 2010 bankruptcy and assumed it’d been erased. Then he discovered that a debt collector was seeking more than double the $75,000 he’d originally borrowed. That kind of hit would wipe out much of the equity he wanted to tap.

“I just couldn’t believe it,” Murphy said. “How did this happen?”

Like thousands of other homeowners across the US, Murphy was blindsided by a “zombie second mortgage.” These loans were taken out before the 2008 housing market collapse and laid dormant for years. Debt buyers bought them up for pennies on the dollar and later shocked homeowners with huge bills inflated by years of back interest.

The story of how these mortgages lingered so long, without borrowers knowing, begins with the messy and incomplete cleanup of a once-in-a-century economic catastrophe. After home prices plunged, the US government and banks spent billions of dollars modifying primary home loans for struggling borrowers but left vast numbers of second mortgages intact. As the housing market recovered, those loans became valuable again, setting ticking financial time bombs for home owners across the country.

“Even after all the efforts by government and industry to reduce needless foreclosures, the potential for zombie second mortgages remained unresolved,” said Patricia McCoy, a law professor at Boston College who helped set up the Consumer Financial Protection Bureau.

Murphy’s case captures much of the post-crisis chaos, involving a foreclosure, bankruptcy, mortgage-backed securities, bond insurance and byzantine rules about when lenders have to send statements. It was so convoluted that even the firm that ended up with his loan said it went years assuming it had no claim to his property. Only in 2024, after Murphy contacted the company about the lien, did it assert that the debt was still valid.

Shawn Murphy, at the home where he lives while being deployed, near Camp Humphreys in Pyeongtaek, South Korea. Photographer: Woohae Cho/Bloomberg

Second mortgages helped fuel the housing bubble and, by the time the market collapsed, Americans had more than $1 trillion of them outstanding. More than 9 million of the loans were taken out between 2004 and 2008, according to federal data. But when the crash came, homes weren’t worth enough to make foreclosure an option for second mortgage holders, so these debts became a lower priority for regulators than primary mortgages.

About 165,000 loan modifications were started through the main federal initiative for seconds. The government also secured a $25 billion settlement with the five biggest mortgage servicers in 2012 over their alleged contributions to the crisis, including widespread “robo-signing” of foreclosure documents. This led to just over 220,000 junior mortgages getting modified. Tens of thousands more were wiped out.

One roadblock to helping more consumers get relief from second mortgages after the crisis was officials’ fear that erasing the loans would put big banks under too much stress, according to a congressional oversight report.

At the end of 2008, the Big Four — Bank of America Corp., Citigroup Inc., JPMorgan Chase & Co. and Wells Fargo & Co. — held about $475 billion worth of second mortgages, according to reports submitted to the Federal Reserve. Because many of these debts were underwater and posed a threat to lenders’ stability, federal officials allowed banks to delay an accounting hit on the debts, according to Arthur Wilmarth, a law professor who was a consultant for the Financial Crisis Inquiry Commission, which Congress created to write the official federal account of what caused the 2008 crash.

“It was a form of extend-and-pretend,” said Wilmarth, an emeritus professor at George Washington University. The regulators realized that if they didn’t go easy on the banks, the resulting holes in their balance sheets could have triggered another round of bank bailouts, he added.

Eventually, the banks and other financial firms cut their losses by selling the loans for a fraction of their face value without lowering the amounts borrowers owed or forgiving them completely. By the end of last year, amid a broader pullback in their mortgage lending, the four banks held just over $60 billion of second home loans.

These sales seeded many of the debt buyers that would scoop up zombie mortgages and, years later, try to collect on them. Disputes over these mortgages have led to scores of private lawsuits. Borrowers have produced evidence that they said shows debt collection firms violated consumer-protection laws by failing to send regular statements and demanding repayment beyond statutes of limitations.

By 2023, federal regulators had begun investigating companies involved in zombie mortgages for such alleged violations, according to two people with direct knowledge of the effort. Those efforts stalled when the Trump administration gutted the CFPB, though a spokesperson told Bloomberg in September that they have not been abandoned.

Senator Elizabeth Warren of Massachusetts, the ranking Democrat on the Banking Committee, sought information this week about whether banks forgave loans under their settlement obligations then sold the same debts to companies that are now seeking to collect.

In interviews, three executives and a consultant involved in cleaning up the mortgage mess at the biggest banks in the years following the crash acknowledged that they helped create the conditions for the zombie loan problem. All asked not to be identified to protect professional relationships. As one described it: We “put a lot of these guys in business.”

Shawn Murphy’s duplex in Los Angeles. Photographer: Leafy Yun Ye/Bloomberg

Few companies better illustrate the excesses that helped precipitate the financial crisis and Great Recession more than the lender Murphy used when he refinanced his home in 2005. At the time, Countrywide was the nation’s largest mortgage lender. It later settled federal and private lawsuits over allegations that it steered minorities into higher-cost loans and misled investors about the quality of the mortgages it originated.

On a modest Army Corps salary, Murphy somehow qualified for two loans on his duplex. The first mortgage, for $600,000, allowed him to decide how much he paid each month, even if the amount was less than the accruing interest. His $75,000 second mortgage started out with a 9% rate that could float as high as 18%, documents reviewed by Bloomberg show.

Like most of Countrywide’s loans, both debts were quickly sold off to feed Wall Street’s booming business of packaging mortgages into bonds, known as mortgage-backed securities. But the rights to service the loans — that is to handle day-to-day administration, like sending statements and receiving payments — remained with the company.

BofA acquired Countrywide and those servicing rights in July 2008, as the business began to unravel amid mounting defaults. Eventually, the bank would suffer tens of billions of dollars in losses from home loans the mortgage company had approved. As BofA executives dug into the lender’s books and started facing lawsuits from investors over the bad loans Countrywide had packaged into bonds, the bank’s senior leadership went into damage control.

“The conversations were really about managing and mitigating the losses,” said a former senior BofA executive, who participated in C-suite conversations.

Meanwhile, the Obama administration was pushing the big banks and servicers to modify people’s loans and slow the nationwide surge of foreclosures. More than $30 billion in federal funds were spent to help homeowners.

From the outset, though, the Treasury Department’s flagship Home Affordable Modification Program, or HAMP, was a magnet for criticism. It was complex, and stories of lost paperwork and other bank errors were legion. A companion program focusing on second mortgages, called 2MP, was slow to start and ultimately modified far fewer loans than HAMP.

Two former executives who oversaw BofA’s effort to implement the programs and manage its bad loans described operational chaos. The bank’s call center staff were poorly trained and operated in silos, they said. That likely led some homeowners to believe their second mortgages were getting modified along with their first loans, one of the people said.

Another person familiar with BofA’s mortgage operation back then said it was a chaotic time at banks and in government, generally. The lender took steep losses when selling the mortgages, mostly to institutional buyers. Other pools of loans had been packaged into securities, and the bank didn’t always control who ultimately bought those mortgages, the person added.

As part of the $25 billion settlement with regulators, BofA canceled nearly 142,000 second mortgages, totalling approximately $10 billion, according to Bill Halldin, a spokesman for the Charlotte, North Carolina-based bank.

Yet, years later, a disproportionate number of Countrywide loans ended up with about two dozen debt-collection firms that have been active in pursuing zombie seconds.

Bloomberg analyzed property records for 5.5 million second mortgages made from 2002 through 2008. Countrywide originated 11% of these junior loans, the most of any company. Yet it accounted for 22% of those that were eventually controlled by the debt collectors — twice Countrywide’s original market share and far higher than any other lender.

Source: Bloomberg analysis of public property records aggregated by Attom Data Solutions

Note: Chart reflects the five largest original lenders in Bloomberg’s analysis. Merrill Lynch bought First Franklin in 2006. It said it would shutter the business in March 2008. Bank of America bought Countrywide later that year and struck a deal for Merrill that closed in 2009.

“The vast majority of these loans were originated before Bank of America acquired Countrywide,” Halldin said. “Following the financial crisis, Bank of America processed more than 1 million mortgage modifications and provided tens of billions of dollars in relief directly to homeowners.”

Murphy got an engineering degree at California State University, Los Angeles, then took a civilian job with the Army Corps in the 1990s.

He concedes that, like many Americans in the mid-2000s, he took on far more debt than he could manage. Lenders just kept giving him money. He financed two condos and a house, in addition to the duplex. Some of these loans, he said, were taken on to help family members.

As his debts piled up and the US plunged deeper into recession, Murphy began a series of assignments that took him away from LA. These included time in New Orleans after Hurricane Gustav and, later, Afghanistan.

By early 2010, Murphy had fallen behind on the duplex’s first mortgage. While he was overseas, BofA offered to help him catch up on missed payments by adding nearly $111,000 to his principal balance. In a move indicative of the disarray at the time, BofA then foreclosed on that modified mortgage days later.

Murphy declared bankruptcy in November 2010 and began wrangling with BofA. The bank rescinded the foreclosure in 2011 and eventually agreed to two more modifications of his first mortgage. One of them knocked about $136,000 off his principal balance, another more than $82,000.

His second mortgage, meanwhile, had fallen into a black hole.

A Tale of Two Loans

Sources: Loan documents, property records, bankruptcy filings

Note: Chart does not reflect any servicing changes on the first mortgage after 2015 because of incomplete records

Last year, with the help of Denise Wilhite-Thomas, a former mortgage underwriter who now works with borrowers facing foreclosures, Murphy started to gather documents to understand what had happened. These records, along with interviews with people familiar with his loan file, show how he was blindsided by the debt.

In November 2009, BofA subcontracted with a Dallas-based loan servicer called Real Time Resolutions to handle the second loan. In a lawsuit the company filed against a competitor, Real Time said it took over servicing of thousands of delinquent second mortgages at the time. It recently had about 24,000, according to an internal CFPB analysis created as part of its research into zombie mortgages during the Biden administration.

Unlike banks, debt collectors like Real Time weren’t part of settlement agreements regulators reached after the financial crisis that required significant consumer relief. And some of them didn’t participate in federal programs that incentivized loan modifications after the housing market collapsed.

These firms get a share of what they recover, creating a strong incentive for them to collect, according to interviews with people in the industry and servicing contracts reviewed by Bloomberg.

Denise Wilhite-Thomas at her home office in San Ramon, California. Photographer: Rachel Bujalski/Bloomberg

Because of Murphy’s bankruptcy, the rules allowed Real Time to stop sending him statements. He was ultimately discharged, which meant he was no longer personally responsible to pay the loan back. Nonetheless, Real Time said that a lien on his property remained, giving the debt collector a legal claim to it if the debt remains unpaid.

“We paused our statements due to his bankruptcy” and foreclosure, a Real Time spokesman said in a statement. “After that foreclosure was rescinded a year later, Mr. Murphy became the owner again” and never made a single payment on the second, the person added.

It was only last year, after Murphy discovered the lien, that the company began sending him statements again. Real Time said it was under the mistaken assumption that the loan had been wiped out by BofA’s 2010 foreclosure.

More than a decade had passed without regular communication on the second mortgage, but, Real Time said interest kept accruing. By the time Murphy got a payoff quote last year, the company asserted he owed $159,355.

Wilhite-Thomas shows a document rescinding the 2010 foreclosure on Murphy’s duplex. Photographer: Rachel Bujalski/Bloomberg

As the dust settled after the financial crisis, Murphy’s second mortgage and many others ended up with bond insurers. These companies had sold coverage that paid investors if mortgage-backed securities went bad and, in many cases, took control of the underlying loans after paying claims. In 2016, Murphy’s mortgage and others were transferred to a trust that then hired Real Time to collect, according to three people familiar with the transaction and documents reviewed by Bloomberg. It’s unclear how much the trust paid for the loan.

Real Time noted that it offered Murphy a payment plan last year. A copy provided by Wilhite-Thomas shows that it would have required Murphy to put down about $13,000 and make $558 monthly payments for the first year, before reverting to the previous loan terms. Another option the company provided was to pay off the debt in one lump sum. If he chose this, Real Time offered a 1% discount on the balance.

Murphy thought he should get a bigger haircut. Real Time said it rejected his proposal to pay a little more than half.

Murphy has hired a lawyer to weigh his options and determine whether he can challenge the validity of the lien. His sister died last year. He was never able to refinance the duplex, which Zillow estimates is now worth more than $1 million.

He said he regrets taking on so much debt earlier in his life. But he still struggles to understand why there was such a long gap in communication about his old second mortgage. At 58, he wonders how the zombie debt will affect the nest egg he’s building for retirement.

“If they cared about the loan, then they would have contacted me,” he said. “I would have taken care of it.”