New York’s Real Estate Tax Breaks Are Now a Rich-Kid Loophole

If you have a modest income but access to lots and lots of cash, New York City has an apartment ownership program that’s right up your alley. Even if it wasn’t meant for you at all.

The changes at the building in Brooklyn’s Williamsburg neighborhood began in 2009, when a guitar shop owner whose father was a renowned art appraiser purchased a four-bedroom apartment. His mom lent him the money. Then came a writer who borrowed from her mother, a psychologist. A movie production manager and her partner, a photo director, bought their unit with a loan from her father, a physician in Maryland. A flurry of additional purchases without mortgages followed, including by a Shakespearean actress whose father lives in a terraced penthouse overlooking Central Park and a fashion designer whose father is a gynecologist in California.

Similar colonies of young people with creative sensibilities and well-off parents have taken root in Williamsburg for years, but the gentrification of this particular six-story building on South 2nd Street had a surprising set of enablers: the taxpayers of New York. It’s one of about 1,000 properties across the city that receive a special property tax break created to make homeownership affordable for low-income people. The building had income restrictions, and these buyers met them. At the same time, they had access to a lot of cash, which they used to score their units at well below market prices. Never mind their wealth or their parents’; the tax break doesn’t require any limit on assets or preclude gifts.

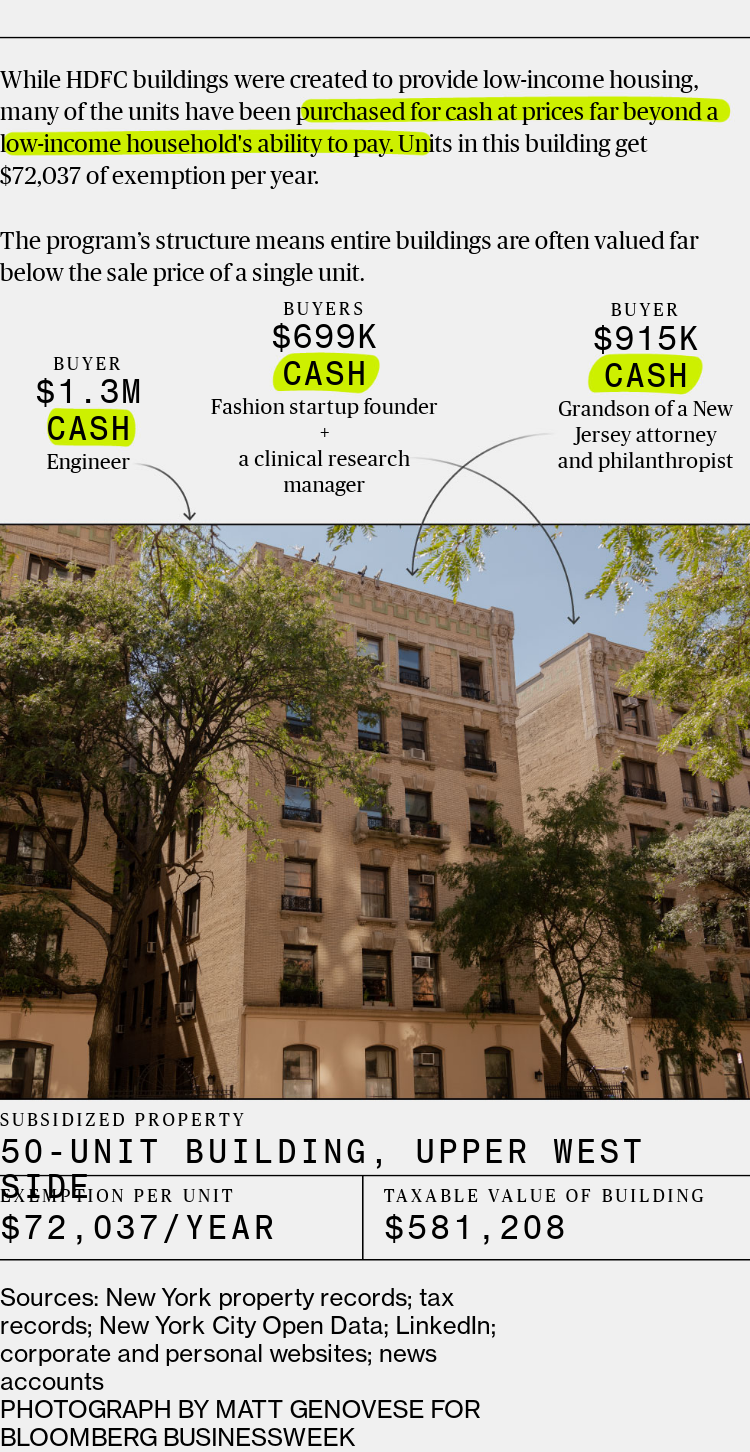

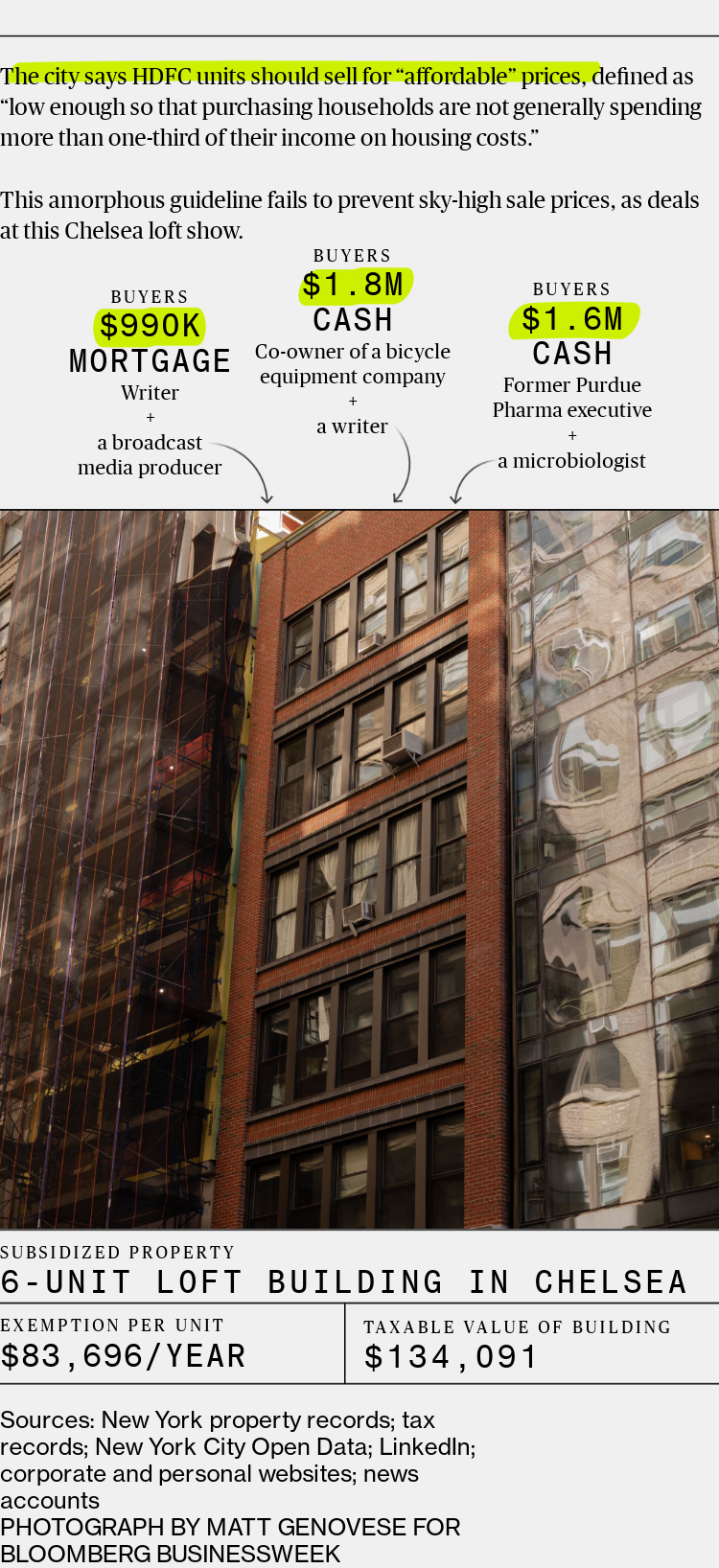

The children of America’s wealthy are quietly sewing up deals like this in some of New York’s most desirable neighborhoods, in buildings known as Housing Development Fund Corporation cooperatives, or HDFCs. These buildings were at one time in financial (and often physical) distress, and many are still shunned by conventional mortgage underwriters—hence the need for buyers to pay cash. Many are no longer cheap, because the agreements that once limited resale prices have expired. But even at prices that can crest well above $1 million, they’re discounted to the market, because of the income limit on buyers and the lack of available financing in some cases. And the taxes can be remarkably low. On South 2nd Street, the owners enjoy annual property tax discounts of roughly 70%.

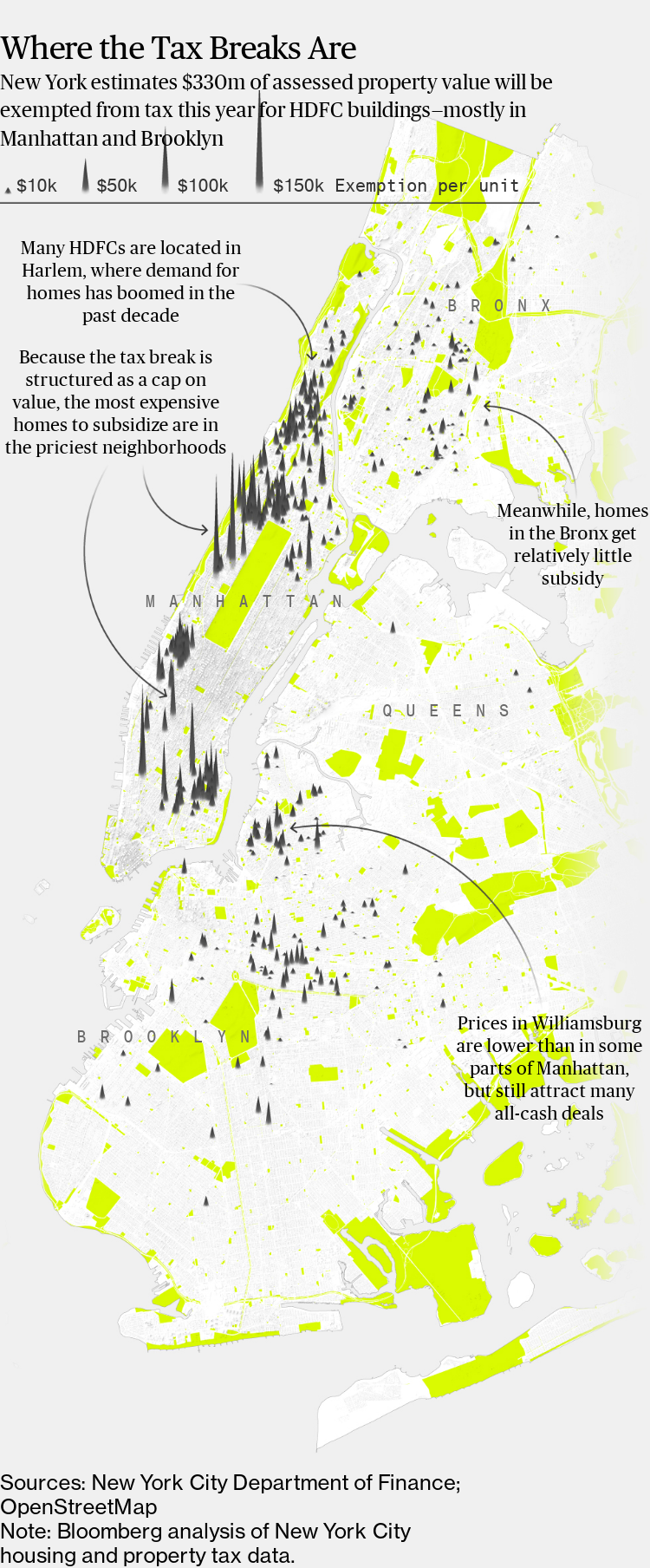

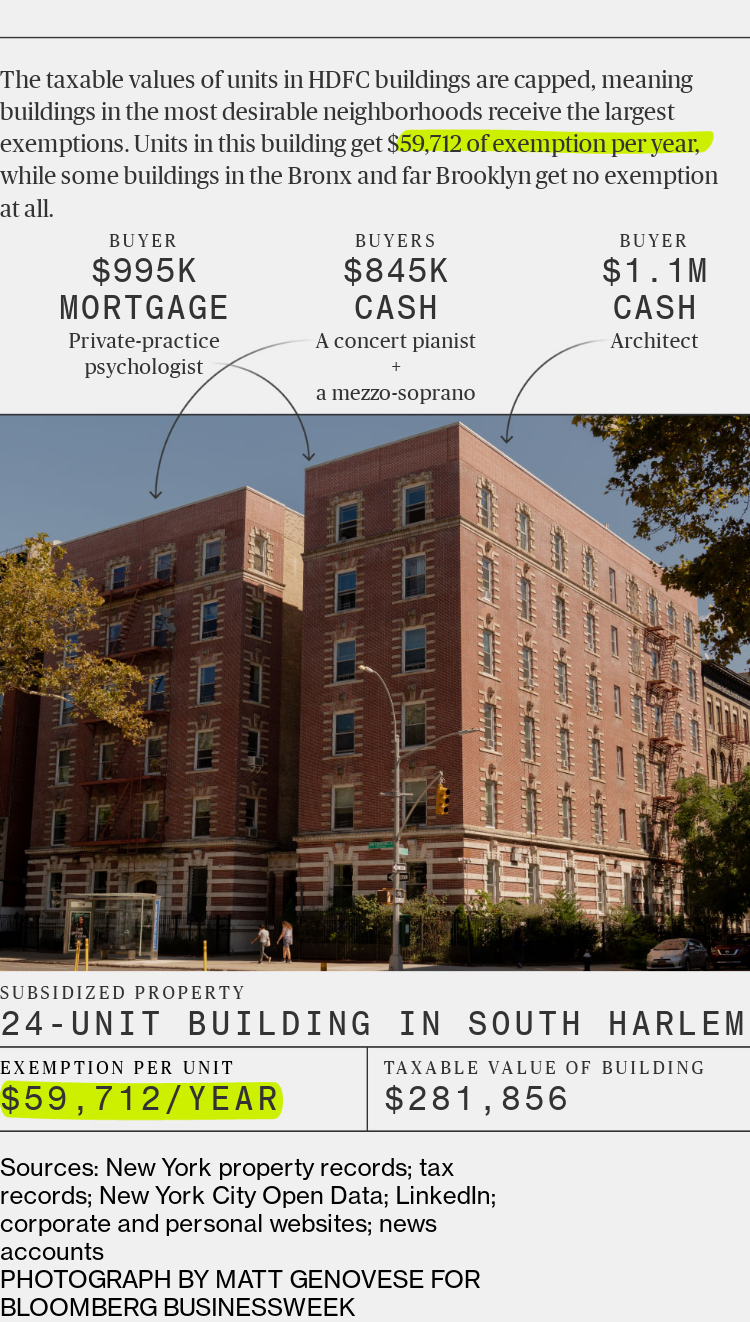

The tax break was designed to be simple—too simple, as it turns out. The program sets a maximum taxable value for every HDFC unit across the city. This year it’s $11,079, in a market where the median price for a home has risen to $770,000. Because of this system, half the aggregate tax benefit will go to the top 20% of eligible buildings by value. Struggling buildings in poorer areas, meanwhile, will get no benefit at all. Their values are too low for the tax break to have any effect, and because of their HDFC status, they don’t get an abatement that most market-rate co-ops receive. Dozens have been foreclosed on in recent years for unpaid taxes.

In short, because of inadequate rules, poor design, and decades of lax oversight, these low-income tax subsidies are being scooped up by the well-to-do. “They’re just gaming the system,” says Penny Gurstein, an expert on affordable housing who directs the Housing Research Collaborative at the University of British Columbia. “This is now just being used as a playground for the rich.”

Across the U.S., studies have shown that local property tax systems, which raise more than $500 billion annually, are deeply unfair, favoring the wealthy and systematically applying higher effective tax rates to lower-valued properties. New York’s outcomes are among the most unequal. But even in a system shot through with inequalities, the exploitation of the HDFC program by affluent bargain hunters stands out.

HDFC sales are infrequent, and not all of them go for big-dollar prices. Nonetheless, it happens often enough that the city’s Department of Housing Preservation and Development acknowledges that “strong reforms are needed.” The agency made a run at that in 2016 but failed in the face of what a spokesman called “strong objections from many HDFC co-ops and their elected representatives.” Since then, the most desirable HDFC apartments, swept along by the forces of the New York real estate market, have only drifted further beyond the reach of the people they were set up for.

An HDFC cooperative exists, per New York state law, “exclusively to develop a housing project for persons of low income.” That doesn’t stop some HDFC buildings from advertising how lax they are about enforcing income limits. Bloomberg Businessweek found dozens of listings dating to 2010 that failed to mention income restrictions for the building or plainly said there were none. A four-bedroom unit at 238 W. 106th St. was listed this year for $1.85 million and advertised as having “no income restrictions,” despite city records showing it benefits from the exemption for low-income housing. The building’s HDFC status lowered its taxable value this year by $3.6 million and cuts its owners’ tax bill by more than $400,000. A building manager at ABC Realty, which manages the building, told Bloomberg Businessweek she would inform the brokers that “they need to be compliant.”

When income limits are enforced, the rules can be as complex and unintuitive as everything else about New York City real estate. Depending on its governing documents, a building will set the limit by various methods. One looks like this: Take the annual common charges for the unit, plus the estimated annual utilities, and multiply that by six (or seven if the buyer’s family is big enough). Then add 6% of the seller’s original purchase price. That’s your income ceiling. Some buildings keep it simpler—and perhaps get to a higher number—by using a percentage of the area median income, or AMI, for the New York metropolitan area. Buildings that are committed to low-income ownership might set the limit at 80% of AMI, which matches the city’s definition of low-income. But an HDFC can go as high as 165% of AMI. This year that translates to $137,940 for a single person and $196,845 for a family of four.

For buildings with high prices and tight income caps, gifting is just about the only way a qualified person can buy some of these apartments, especially if an all-cash deal is necessary. The upshot is that a child of well-to-do parents is something of a perfect buyer.

“They didn’t think about rich kids with a trust fund but who make 30 grand a year working for a nonprofit,” says Matt DeSilva, a real estate agent who specializes in HDFCs. “Because that wasn’t really happening when the program was created.” DeSilva has personal experience with an HDFC purchase. When his mother lent him the money to buy into the building on South 2nd Street in early 2009, he was playing bass in a band and running his small guitar store. He put 20% down from his savings, he says, and sought bank financing for the rest. But because of the 2008 mortgage crisis, he says, a lender that had approved the loan backed out. “In order to make this purchase happen, my parents did me a huge favor and took out a home equity loan in order to give us a loan in the form of a private mortgage,” DeSilva says.

Students at Columbia University and Brooklyn’s Pratt Institute appear frequently among HDFC buyers, as do young adults pursuing passion projects that might pay off someday but haven’t yet: DJing, fine art, influencing, music, modeling, fashion design. Others are future doctors and lawyers. Buyers frequently list their parents’ addresses in upscale suburbs of Los Angeles, Pittsburgh, Baltimore, and other cities on purchasing documents. In extreme cases, cash buyers have ties to the wealthy and powerful. A son of British lord Simon Gavron bought an HDFC unit; a son of former Grumman Corp. Chairman John Bierwirth did, too.

Parents say HDFCs offer financial breathing room for creative children. Jessica Nacheman says a one-bedroom unit on the Upper West Side, purchased last year for $410,000 in cash, “was really kind of a godsend” for her daughter, a 2015 Bryn Mawr graduate and harpist who needed her own place to avoid disturbing roommates with rehearsals. “She had been able to put some money aside, from gifts, etc., etc.,” says Nacheman, who’s worked as a lawyer for a division of Exxon Mobil Corp. and whose husband retired as a principal in an engineering firm. “Now she can go forward with lower maintenance.” Maintenance is a unit’s share of the common costs for a building—staff, water, repair funds, and, significantly, real estate taxes. The HDFC tax break is one reason the monthly maintenance for this apartment was advertised at just $598 at the time of the sale, perhaps half of what it might be in a market-rate building. “It’s really a great program,” Nacheman says.

Other parents are less eager to discuss it. “It was a one-time opportunity,” says Avraham Glattman, a real estate investor, in a brief conversation. Glattman says that in 2016 his business partner, Pete Jacov, found two apartments in a building near Hudson Yards, on the West Side of Manhattan; a son of Glattman’s bought one, and a son of Jacov’s bought the other, for $220,000 apiece, in cash. Jacov hung up when reached by a reporter and didn’t respond to text messages. Both sons are pursuing careers in law.

There’s nothing illegal about taking advantage of rules that offer such obvious benefits for people with cash to burn. And a lot of people might say that if you can find an advantage in the ruthless New York real estate market, you should exploit it. But these subsidized housing cooperatives were never intended to be a windfall for rich kids. They began as part of an historic transfer of wealth that made first-time homeowners of some of New York’s most economically vulnerable people.

In 1970s New York, the economy had collapsed, and slumlords had stopped making repairs on their buildings and paying property taxes. Eventually, officials seized the properties, making city government one of the largest landlords in town. The buildings remained in disrepair, and the city couldn’t afford to fix them. Rather than return them to unscrupulous slumlords, city officials sold them to tenants, typically for $250 per unit.

The buildings were organized as cooperatives, then the dominant form of apartment ownership in New York. But the co-op boards they formed often lacked the expertise to manage the buildings’ finances or upkeep. Education programs offered by the city and affiliated nonprofits received mixed reviews. “The training was very threadbare,” says Glory Ann Kerstein, who’s lived in her HDFC unit since 1982. Unpaid taxes, building code violations, and fines piled up.

Faced with the awkward prospect of seizing the very same properties again, city officials came up with a solution in 1989: a 40-year tax break that would help the cooperatives dig out of debt.

The benefit was structured as an absolute cap on the taxable value of each HDFC unit, set at $3,500 in the first year and climbing on a schedule. That means a four-bedroom in Upper Manhattan (like the one that sold last year for $2.1 million) is taxed the same amount as a one-bedroom in the Bronx. The tax break itself wasn’t made contingent on keeping prices affordable. Some HDFC co-ops signed temporary agreements with the city that included price caps—tied to fixed schedules or complex formulas—but the agreements have been expiring over the years; they’re now in effect at fewer than 25% of HDFC buildings, according to the housing department. The agency says a small number of new cooperatives have been formed with stricter rules around income and assets.

The rise in prices is warping one of the few shields against New York’s exploding housing costs. For working people who made up the first generation of owners, including Black, Puerto Rican, and Dominican families, the buildings offered a chance at economic stability.

As a child, Sandy Baez emigrated from the Dominican Republic to live with his mother in an apartment building in Washington Heights, in northern Manhattan. The property’s absentee landlord had survived previous foreclosure waves, only for the city to seize his three-building complex starting in 1991, just before their arrival.

“It was infested with rats, there were holes in the bathroom ceilings, there was nobody to call for repairs,” Baez recalls. Still, “it was a big improvement from what we had in the Dominican Republic.”

It took more than a decade for the city to officially transfer the deed of the complex to its residents, 66 units for $16,500, in 2003. Over time the new owners pulled together to improve the property. Because the taxable value of the apartments fell below the HDFC cap, the owners didn’t receive any tax relief until 2015—$230 per unit, while far wealthier buildings were reaping millions of dollars. Still, ownership offered tranquility and stability, and Baez and his siblings were able to attend college.

Only a handful of apartments in the complex have traded hands since the buildings became a cooperative, all for under $50,000. Baez would like to see his neighbors get more financial relief from the city, and he’s frustrated that he and they pay the same in tax as owners of wealthier buildings. But he supports the HDFC system. “Can the city do more?” he asks. “I think so. But I believe it works, 100%.”

HDFC units can sell for 50% or less of what a comparable apartment might sell for, depending on factors like the financial and physical condition of the building. Because they are often such bargains, cheating on applications for them does occur, brokers say. “They’ll hand you a tax return that they did on QuickBooks or Quicken or TurboTax,” says DeSilva, the guitar dealer-turned-real estate agent. He’s started asking for tax transcripts from the IRS.

For many buildings, the city doesn’t monitor sales. That leaves agents and the cooperatives to catch dishonest buyers, but they have incentives to see high-priced sales take place. Original owners from the 1980s and ’90s often experience the biggest wealth-creation event of their lives when their unit goes for a high six-figure price; it’s the equivalent of a retirement account. The cooperatives benefit, too; most collect a so-called flip tax of about 30% of the profit when an apartment sells. Big-dollar transactions refill their coffers. (In conventional co-ops, the flip tax typically tops out at 3%.)

The city estimates 27% of HDFC cooperatives are experiencing some form of distress, with many still weighed down with debt or in need of major improvements. For these buildings, it’s almost impossible to resist the transition from low-income owners to wealthier buyers. They need the flip-tax money.

Clara Meregildo knows how unsettling these pressures can be. At her seven-story prewar building about four blocks north of Central Park, seven units have traded for cash since 2018 at an average price of $339,000. The flip taxes have helped chip away at the building’s debt, but it still stands at close to $650,000. There are uncomfortable questions about the building’s future. “I’m committed to keeping the building affordable,” says Meregildo, a human resources professional who bought a unit in 2007 and serves on the co-op’s board.

Fellow board member Jeremy Fenn-Smith, who bought in 2003, predicts it won’t be easy, thanks in part to the building’s present reliance on cash sales. People who are paying cash to get in now, he says, won’t be interested in limiting their resale options. “The idea is that everybody has a three-bedroom, large unit close to the park; they’re not going to want to have caps on that. They’re certainly not low-income people. We have racial diversity, we have economic diversity. That will change. I think that’s inevitable.”

On the other side of the block, in a 24-unit HDFC building, recent sales have topped $1 million. Only three apartments are still held by original owners. Thanks to the HDFC tax break, the entire property’s taxable value is $281,856. Bart Platteau, a Belgium-born jazz flutist who owns a unit in the building, says it doesn’t make sense for him and his new neighbors to be receiving a tax break for low-income housing. But he isn’t suggesting giving up something for nothing.

“Don’t give them the tax breaks, but let them be free, and let them be regular co-ops,” Platteau says.

That idea is gaining traction in HDFC buildings, in part because many owners believe their units’ value would spike if income caps were lifted. The New York State Office of the Attorney General isn’t encouraging the hope. In 2015 it issued guidance to local officials that says the law prohibits HDFC buildings from reorganizing as market-rate co-ops in most circumstances.

An interest group called the HDFC Coalition is attempting to fight that. John McBride, a leader of the group, says the organization believes most HDFC coops “want and need to remain incorporated as HDFCs so long as a sufficient tax break is in place to keep monthly housing costs affordable.” At the same time, he said, the group insists on “maintaining our right to dissolve our HDFCs and convert to normal co-ops, if only to keep city government from taking over our private homes.” He questions whether city officials who set HDFCs in motion really intended for them to be regulated in perpetuity, and says the larger policy goal was to transfer hundreds of often stressed and dubious buildings off the city’s books and into stable, private hands. If the original HDFC owners hadn’t been willing to take them on, many of those buildings would have been abandoned, McBride contends. “HDFC shareholders saved these buildings, and these buildings belong to us and always will,” he wrote. “Period.”

The coalition wasn’t always so interested in laissez-faire principles. At its founding, in 1992, one of its leaders was Jordi Reyes-Montblanc, a West Harlem community activist who told the New York Times in 1998 that HDFCs are “intended to be the permanent homes for the self-supporting working poor and low- to moderate-income families.” The units “are not intended to be investment property or for market speculation,” he said.

Last year, Harvey Epstein, a State Assembly member for eastern Manhattan, drew the ire of the HDFC Coalition after crafting draft legislation that would create an HDFC ombudsman’s office, which the group saw as government overreach. He’s still working on a way to reform the law governing the co-ops, but he’s come around to seeing the inevitable trajectory the most expensive units are on: “I’d rather let them go and make them pay full fare,” he says, meaning the co-ops would lose their property tax subsidy. “Units that are selling for $1 million now, it’s hard to re-regulate that back.”

Deregulating the most stable and expensive buildings could spell windfalls for those who’ve played the system artfully, the final move on their way to achieving unfettered price velocity. Epstein thinks state law can be amended to prevent the problem from spreading across other buildings.

If the system is left unchanged, it isn’t hard to envision a future in which gentrification fans out across more and more neighborhoods and their HDFC cooperatives. Hardly a surprising outcome in New York real estate, where the logic of the market wins more often than not. At least there’s a consolation prize: tidy nest eggs for exiting owners, as their homes and city are cleared for the affluent.

(Corrects to provide additional context in 11th paragraph about the buyer of an HDFC apartment in 2009, including information provided after publication.)