Management & Work | The Big Take

The True Cost of Firing a CEO

When a company abruptly ditches its CEO, the costs of the shakeup can quickly add up.

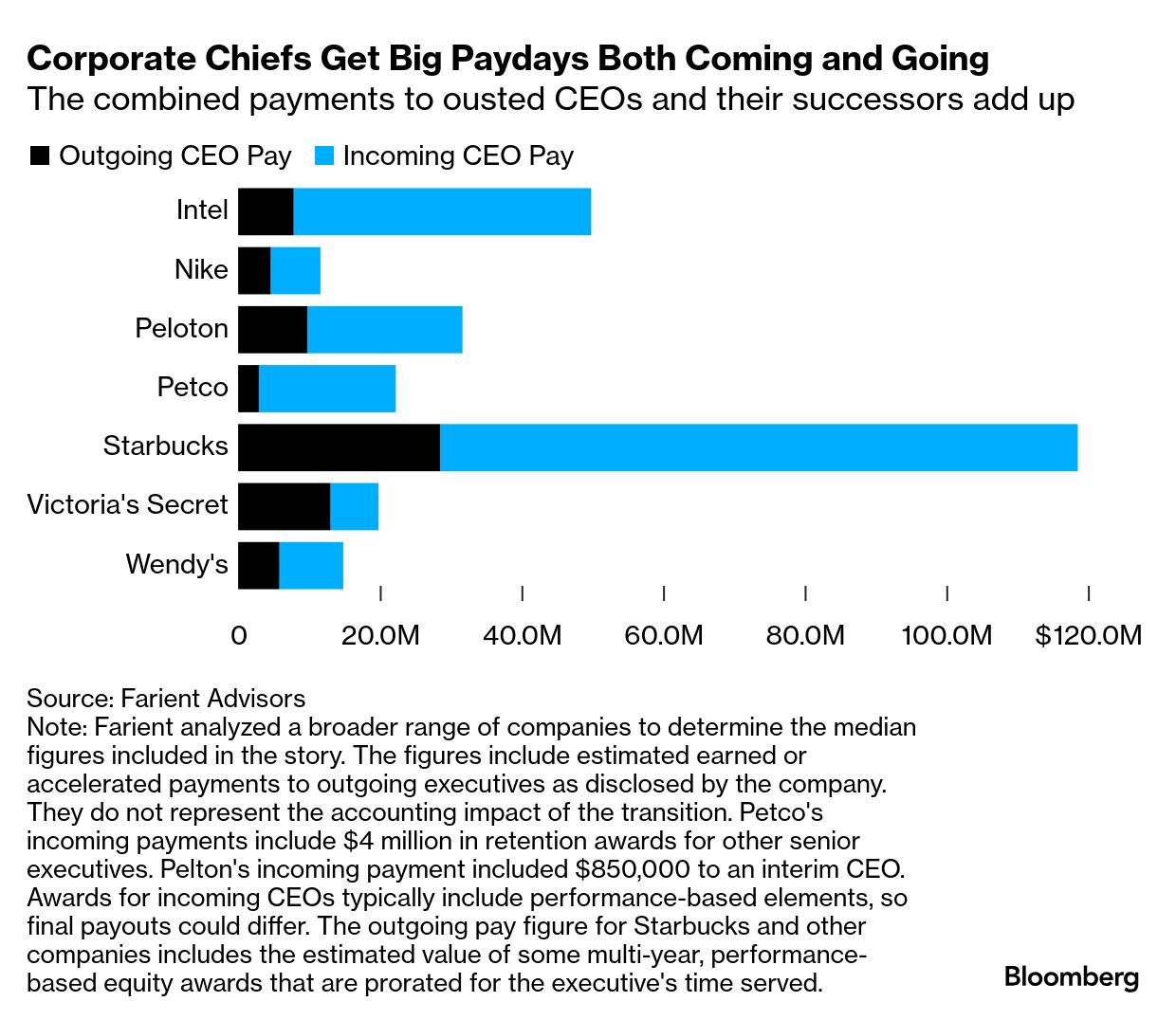

When Starbucks Corp. tapped Brian Niccol as chief executive officer in 2024, it cited the “critical need for a transformative leader” in justifying the hire. If performance significantly improves, stock payouts mean the corner-office switch could cost the company $130 million.

That figure includes estimated exit payments to outgoing CEO Laxman Narasimhan as well as so-called “make whole” awards of cash and stock sufficient to entice Niccol to leave his job running Chipotle Mexican Grill Inc. Starbucks deemed the payments “necessary” to recruit Niccol. But some observers balked.

“The price of the transition is staggering,” concluded proxy-advisory firm Glass Lewis, in a February report that criticized the company’s succession planning and urged shareholders to vote against its executive compensation plan. “Shareholders should be critical of the costly nature of a CEO transition.”

They rarely are, though. Starbucks’ shareholders approved the pay packages at the company’s annual meeting in March, displaying the same optimism in Niccol’s turnaround ability that lifted the company’s shares 25% on the day his appointment was announced.

Perhaps if shareholders knew the full cost of a CEO ouster, they’d be more wary, as the price tag goes well beyond severance and sign-on payments made public in filings. There’s been increased turnover in the top job, much of it unplanned. According to Exechange.com, there were 134 CEO force-outs last year at Russell 3000 firms.

CEO Ousters Are On the Rise

Force-outs picked back up after a lull during the pandemic

To give a proper accounting for unplanned CEO departures, Bloomberg News consulted with compensation consultants, academics, corporate lawyers, executive-search advisors and public-relations experts. Farient Advisors, an executive compensation and corporate governance consultant, crunched the numbers and provided estimates based on a sample of last year’s departures at big US firms like Starbucks, Intel Corp. and Nike Inc.

Deciphering the convoluted payments to the outgoing and incoming CEOs was just one element of the analysis. Corporate boards typically hire a bevy of advisors to handle the hunt for a new CEO and other critical aspects of the transition. Tasked with working fast and under scrutiny, none of them comes cheap. Sometimes boards also give retention bonuses to other senior leaders during the transition. The new CEO might then bring in fresh C-suite members, which results in additional replacement costs. (Niccol’s new chief financial officer, Cathy Smith, received cash and stock worth an estimated $11.4 million to come aboard at Starbucks.)

Other indirect costs of a CEO ouster are harder to measure, but still very real, like the impact on employee morale, productivity and turnover, or business opportunities that might get sidelined when the board is consumed with finding a new chief. And then there’s the potential hit to the stock.

As with layoffs, which Bloomberg analyzed last year, the true cost of a CEO ouster is rarely straightforward, but always steep.

Unlike Kohl’s Corp.’s recent firing of CEO Ashley Buchanan, who was found to have channeled millions of dollars of business to a paramour, most CEOs are rarely fired “for cause,” a determination reserved for especially egregious behavior. Often, CEOs who know they’re in danger will voluntarily (and quietly) resign to save face. A formal “retirement” can also mask a firing. Companies are not always required to disclose the true reason for a departure, so lawyers and public-relations reps often work hard to make a dramatic ouster look like a ho-hum transition.

To help determine whether a CEO was actually forced out, we relied on the experts at Exechange.com, whose analysis of leadership transitions cuts through corporate jargon and platitudes like “pursuing other opportunities” to determine the true cause of an executive exit. Exechange scores executive departures on a scale of 0 to 10. Those with a score of 8 or higher are considered to have been forceouts or firings.

Along with Starbucks, other high-profile companies that dumped their CEOs in 2024 included Nike, Wendy’s Co., Peloton Interactive Inc., Under Armour Inc. and CVS Health Corp. The pace of push-outs has accelerated since then amid the tumult of tariffs, uncertainty about the coming impact of artificial intelligence and other boardroom anxieties, with 42% of 157 departing CEOs being forced out or fired in the first half of 2025, Exechange data show. That’s up from an average of about one in three over the previous eight years.

“In the current environment of rapid technological advancement and geopolitical volatility, boards are rigorously replacing CEOs who are not up to the new challenges,” said Exechange founder Daniel Schauber.

1.

Payments to the exiting CEO

Once the board decides to make a switch — often in an emergency meeting — the costs start accruing. Public-company executives typically receive at least a partial payout of unvested stock awards if they are terminated without cause. Farient’s analysis of CEO push-outs in 2024 at a sample of more than two-dozen Russell 1000 index firms found that about three-quarters of companies accelerated some equity payments for outgoing CEOs. (Sometimes, CEOs will receive short-term “advisory” contracts purportedly to smooth the transition to the new leader, but they’re often just hanging around to continue to vest their equity.)

Some CEOs are sent packing with the promise of assistance from outplacement firms or other career advisors, according to Robin Ferracone, Farient’s CEO. Sima Sistani, who was ousted in 2024 from WW International Inc. (formerly known as WeightWatchers), walked away with up to $37,500 in executive coaching.

Often these benefits are built into the executives’ employment contracts. It’s not uncommon, though, for departing CEOs to try and capitalize on the urgency of the situation and negotiate for more severance or other perks, according to Helenanne Connolly, a partner at the law firm Cooley LLP who represents corporate clients.

Severance arrangements for CEOs can vary widely, and often aren’t directly correlated to a company’s size or industry. Farient’s analysis of ousters in 2024 found companies paid a median $3.1 million in cash. For those paying out equity, the median total payment landed at $6.2 million. All to say goodbye to someone who, in most cases, screwed up.

Narasimhan, after leaving Starbucks, is due to receive more than $9 million in cash, and the company estimated his potential equity payout at just under $20 million, according to its regulatory filings. Not bad for 17 months’ work. (The actual value won’t be finalized until the company’s 2026 fiscal year concludes, due to some multi-year performance awards that extended past his departure and will be prorated by his time served during those periods.)

2.

Payments to incoming CEO

Finding a new CEO to right the ship is an even steeper cost when the board is in a rush. The main reason: make-whole payments, which seek to replace the estimated value of the cash and stock that the incoming chief is sacrificing at his or her old employer.

In Niccol’s case, the make-whole payments — $10 million in cash and $80 million in equity — were “mammoth,” according to Glass Lewis. What’s more, the proxy-advisory firm said it’s not entirely clear how Starbucks arrived at its estimate for what Niccol was giving up, which was one reason why it recommended a vote against Starbucks’ compensation plans.

Estimating what any CEO might have stood to make based on performance at their previous employer is subject to interpretation. Starbucks, for its part, said the make-whole payment to Niccol covered forfeited grants that would have been paid not long after he departed Chipotle.

“We brought in a proven leader with a strong track record to set Starbucks up for success and create long-term value for all stakeholders,” a Starbucks spokesperson said in a statement. “He is backed by an experienced team, and much of his compensation is tied to future financial performance.”

Corporate Chiefs Get Big Paydays Both Coming and Going

The combined payments to ousted CEOs and their successors add up

While Niccol’s big payday was an outlier, Farient’s analysis found that the median sign-on payment was $9 million, which again is just the enticement to pry the new CEOs from their old job. It doesn’t include their first-year salary or bonus in the new job. These amounts are often comparable to what the previous CEO was making. (Niccol’s performance-based cash bonus in his first year could be as much as $7.2 million.)

What tempers those payments are instances where the new CEO isn’t an external hire, like Niccol or Intel’s Lip-Bu Tan was, but promoted from within, as was the case at discount chain Dollar Tree Inc. and technology manufacturer Jabil Inc. Still, though roughly half of the new CEOs in Farient’s analysis were internal promotions, three-quarters of all the new CEOs received some sort of sign-on award.

3.

Payments to Other Executives

CEO transitions don’t happen in a vacuum — they impact other leaders across the organization. The board might be concerned about losing other members of the C-suite who were staunch allies of the deposed CEO or who perhaps felt they deserved the top job. Other times, retention bonuses go to leaders who step up as an interim CEO while the board searches for a permanent replacement. In those and other cases, boards will hand out retention awards of cash and stock to one or more senior executives.

Those payments can add up: At health-care company QuidelOrtho Corp., for instance, retention bonuses paid to five separate senior executives totaled $6.8 million. Kibble retailer Petco Health & Wellness Co. pledged to pay $4 million “to establish continuity among key members of the leadership team during our search for a permanent CEO.”

That sought-after continuity can be fleeting, though. In Petco’s case, none of the three executives who were granted retention awards stayed long enough to fully vest and as a result received just a fraction of their potential payout. Their departures, in turn, necessitated exit payments and recruitment expenses of their own, compounding the cost of the CEO ouster even further.

Let’s not forget the executives left standing when a CEO jumps ship, as happened at Chipotle when Niccol resigned. The restaurant chain delivered retention awards valued at $38 million to a half-dozen leaders for their service “during the period of uncertainty that inevitably follows a change in top leadership,” it said in a filing.

“The executive ranks get demoralized, they’re bombarded with job offers, and everyone is nervous about the new CEO,” said Joseph Fuller, a management professor at Harvard Business School. “Nobody in their right mind thinks they are in a secure position.”

4.

Payments to Advisers

Finding the new CEO, negotiating his or her new contract and communicating the change in leadership to investors, the media, employees and other stakeholders are tasks typically delegated to outside experts.

The process often starts with an executive search firm like Spencer Stuart, Korn Ferry or Russell Reynolds Associates, whose partners specialize in specific industries and maintain vast networks of seasoned executives, up-and-coming leaders and corporate directors. A search firm’s standard fee is one-third of the total cash compensation (salary, bonus and sign-on payment) paid to the CEO in the first year, though some clients prefer to negotiate a fixed fee instead, according to search-firm executives who requested anonymity to discuss the inner workings of their firms.

With CEO pay skyrocketing — median compensation for the 100 highest-paid CEOs at companies with at least $1 billion in revenue rose 22% to $30.9 million last year, according to pay consultant Equilar — it’s not unusual for a big-company search to cost $3 million, according to one executive recruiter who’s worked on many CEO searches. A few even reach $5 million.

Ousting a CEO can prompt the departures of other senior leaders. One study found that an external CEO hire leads to more than double the rate of C-suite departures than if the new CEO is an internal pick. At Nike, more than half the members of the senior leadership team are new to their jobs since Elliott Hill replaced John Donahoe last year.

On top of that, search firms do more than search nowadays: Many tout their “leadership advisory” services, providing everything from succession planning advice to CEO coaching and onboarding. For that ongoing, longer-term work, they can charge between $250,000 and $500,000 a year, the veteran search consultant said.

Then there are lawyers, who handle everything from assuring regulatory compliance to drafting non-compete agreements to hammering out the new CEO’s contract. At $2,000 an hour, those costs can sometimes reach into the seven figures. Compensation consultants — like Farient — are often employed to provide guidance and analysis on the CEO’s pay package. Crisis communications experts will help get the company’s message (or spin) out, often at $1,000 an hour.

Clients “usually want you 25 hours a day and eight days a week,” said Davia Temin, founder and CEO of crisis-communications firm Temin & Co. A CEO ouster and replacement “will take even more time,” she added. How much more? Temin shrugged: “I can’t even begin to estimate.”

The point is, anything can happen, and the advisers’ job is to make sure it doesn’t leave the boardroom and harm the company’s reputation.

Dramatic ousters over the decades illustrate the risks. The 2005 firing of Carly Fiorina by the board of Hewlett-Packard Co., soon followed by a spying scandal that involved board chairwoman Patricia Dunn, tarnished the legacy of one of the original pioneers of Silicon Valley. Almost 20 years later, Nike’s reputation declined by 6 points on a 100-point scale during its 2024 succession surprise, according to RepTrak, a reputation research and advisory firm.

“Public-company CEO exits often have unanticipated left turns, which require nuanced and thoughtful coordination on several fronts,” Connolly, the lawyer at Cooley, said. “Legal, investor relations, public communications, human resources, tax and finance elements are usually involved, and the pace of these exits is typically accelerated and unforgiving.”

5.

Lost shareholder value

Finally, there’s the hit that investors take.

A 2015 study by PwC’s “Strategy&” consulting unit estimated that forced turnovers at the world’s largest public companies cost each firm an average $1.8 billion in foregone shareholder value. PwC analyzed CEO transitions at 2,500 listed companies across three years to determine the figure, which it calculated from median shareholder returns, relative to the index they traded on, in the year before and after each switch. Its conclusion: “There’s a stark difference between companies able to plan their turnovers and those forced into them.”

Another study, by FTI Consulting, found that news of a CEO shake-up made investors more than twice as likely to sell shares in a given company as they were to buy them. And nearly 40% of investors in the same survey said they would sell a stock solely on the basis that a CEO was new.

Even if a company’s stock price rises when a new CEO is named, as happened at Starbucks, the shares have likely suffered in the months or years leading up to the switch as the company floundered under previous leadership. And don’t read too much into any one-day gains when the new CEO is announced: Since Niccol officially started on the job at Starbucks, the coffee chain’s shares are essentially unchanged.

Starbucks Stock Over Two Leadership Transitions

When it comes to CEO ousters “institutional investors and hedge funds tend to get nervous” that a board under pressure could make another bad pick, said Fuller, the management professor.

That anxiety should extend to the board itself. A CEO ouster might signal that the board needs to change its composition, its advisors or its overall approach, according to Ashley Summerfield, leader of the global CEO and board practice at the leadership search and advisory firm Egon Zehnder. There’s a cost for that as well, but Summerfield believes it can pay off in the long run.

“A CEO ousting is a window into the governance at a company,” he said. “It has costs, but what worries me more is companies that don’t fix their governance in light of the ousting. If it takes a board three years from the first amber lights flashing to get rid of their CEO, why did it take that long? And why were the lights amber, and not red?”

At Kohl’s, the board missed warning signals about Buchanan, according to Blue Heron Research Partners, which analyzes management teams on behalf of investors and found that there were concerns about the former CEO’s business judgment in prior roles with other retail chains. Now, Kohl’s is replacing its CEO for the third time in as many years — an expensive proposition for any big company.

Major search firms typically offer to do another search for free if their initial recommendation flames out within the first year of employment. But after the misstep with Buchanan, Kohl’s was considering hiring a new search advisor.

As the retailer’s board weighs its options, sales remain lackluster, along with employee morale, and the stock is well off its price from the start of the year. And no matter who is eventually hired as CEO, there will be another steep price to pay.