Global investors are looking at the 54 nations that make up Africa with fresh eyes, not only for their vast natural resources but also for the region’s role in the realignment of trade worldwide.

Tens of billions of dollars have been invested in the continent’s industries so far this year—from agriculture to data centers—with more expected as US President Donald Trump’s tariffs reshape global alliances. In the first half of 2025, China inked $30.5 billion in construction contracts with African nations, including railways in Nigeria and ports in Egypt, spending almost five times more than during the same period last year, according to a report from Australia’s Griffith University and China’s Green Finance & Development Center. Government bodies and businesses in Asia, Europe and the Middle East are also plowing money into African countries, some of which, including Egypt and Kenya, have US-reciprocal tariff rates of only 10%. (India’s, by comparison, is 50%.)

The appeal is clear: Africa is home to the world’s youngest population and some of its fast-growing economies. The International Monetary Fund projects it will grow faster than any other region over the next five years. The African Continental Free Trade Area (AfCFTA), officially introduced in 2021 and expected to be fully operational by 2035, is forecast to become the largest free-trade bloc in the world, unlocking access to a $3.4 trillion market. In November an African nation will host the Group of 20 leaders for the first time, in Johannesburg. A country on the continent has never held the Olympic Games, but Formula One is eyeing Africa again after more than 30 years.

Yet while Africa is increasingly relevant in global trade, entertainment and politics, there are also risks for investors. The continent is facing an infrastructure financing gap of as much as $108 billion a year, according to the African Development Bank, including a shortage of roads, navigable rivers and power. Policy uncertainty, skill gaps, high youth unemployment and rising debt burdens are also challenges in many of its economies. Of course, every country and sector is distinct. “Successful engagement in Africa necessitates a nuanced, long-term perspective,” says Akin Dawodu, Citigroup Inc.’s banking head for sub-Saharan Africa.

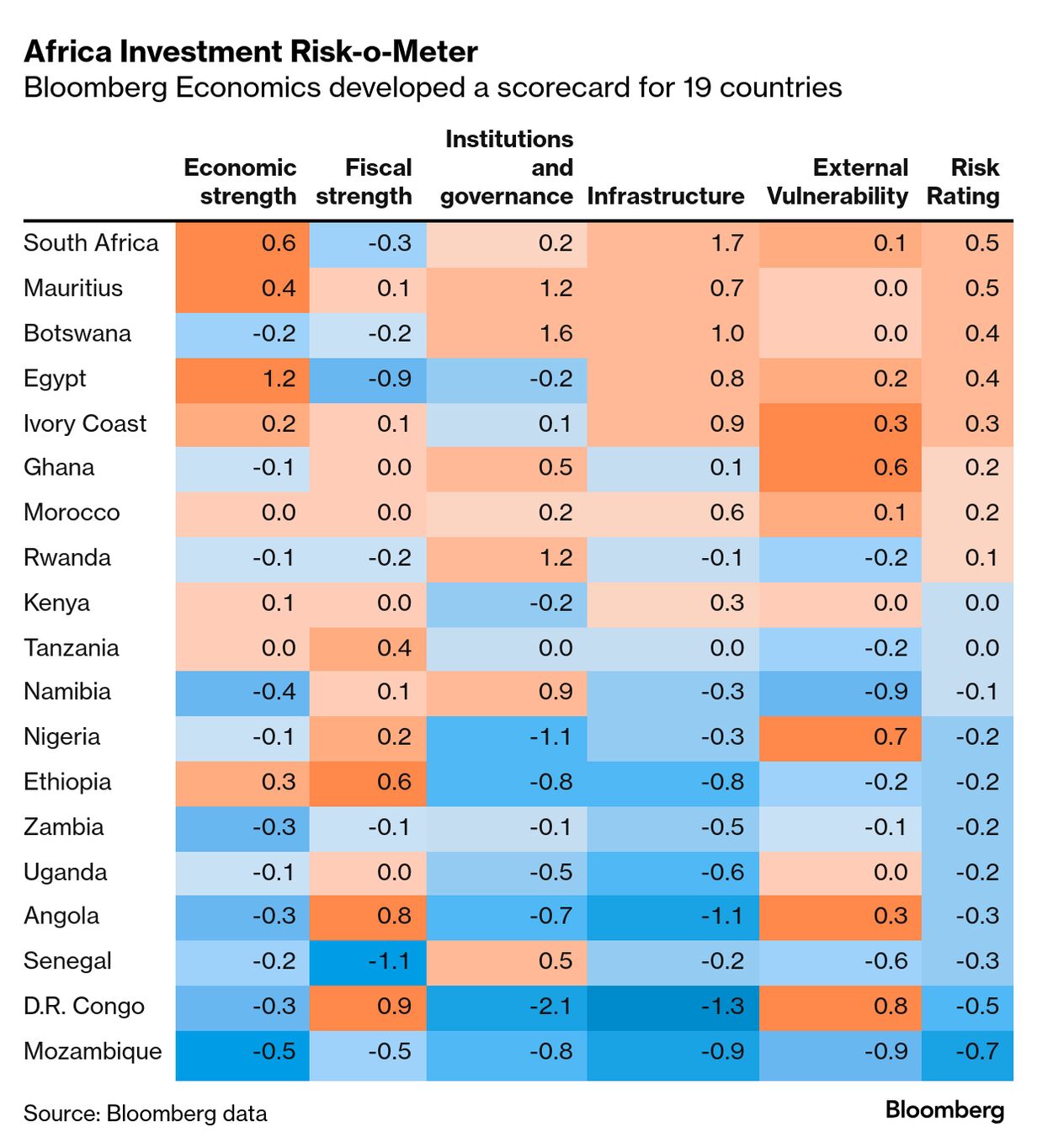

To help investors understand the industries and locations where they might deploy their capital, Bloomberg Economics developed a scorecard for 19 African countries, assigning risk ratings based on five key factors: economic strength, fiscal strength, institutions and governance, infrastructure, and external vulnerability. The risk-o-meter draws on World Bank and IMF data, incorporating dozens of indicators such as gross domestic product per capita and logistics performance, which allow investors to determine the attractiveness of countries based on their own risk tolerance. The list includes Africa’s largest economies, plus several others that stand out for features that tend to attract investors like rich commodity reserves, established financial hubs and thriving business tourism centers. A larger number, denoted in orange, signifies lower relative risk.

Africa Investment Risk-o-Meter

Bloomberg Economics developed a scorecard for 19 countries

Source: Bloomberg data

Bloomberg Businessweek also spoke to investment agencies across the continent and tracked deal flows in key sectors to round out our inaugural Investor’s Guide to Africa. The analysis focuses primarily on the industries on the rise in the most investable countries. This list is in no way comprehensive, but it’s indicative of the kind of deep-pocketed money that’s making inroads in the world’s second-most-populous continent. Despite navigable risks, Dawodu says, Africa has been firmly established “as a critical and exciting frontier for global capital.”

Sector

Agriculture

The Key Number$1 trillionAfrica’s expected annual agricultural output by 2030*

Who’s Investing?

Al Dahra, Citic Construction Co., Power Construction Corp. of China

Investment Case:

The agriculture sector is one of the largest untapped opportunities in a continent that holds about 60% of the world’s uncultivated arable land, especially given rising demand for food, growing urban populations and regional trade integration. Depending on the country, investors can take advantage of tax incentives, long-term land leases, loan guarantees, grant finance and special economic zones (SEZ) for agriculture designed to spur more value-added food manufacturing and processing.

Risks:

Africa’s agricultural promise is undermined by weak infrastructure and increasingly unpredictable weather. Droughts, floods and erratic rainfall threaten harvests and food security.

Some Countries to Watch:

The world’s largest cocoa producers, Ivory Coast and Ghana, are scaling up processing with new industrial complexes. Nigeria’s vast consumer market is driving investment in rice and cassava processing, and Kenya, Morocco and Uganda are expanding their edge in horticulture and exports. Angola and Zambia are opening up vast tracts of farmland to investors, and South Africa remains a key anchor in agro-processing and food retail in the continent.

The Key Number30%Share of the world’s proven critical mineral reserves held in sub-Saharan Africa*

Who’s Investing?

BHP Group Ltd., Glencore Plc, Sinomine Resource Group Co.

Investment Case:

Global revenue from cobalt, copper, lithium and nickel alone are projected at $16 trillion over the next 25 years, according to the IMF. Sub-Saharan Africa could capture more than 10% of that windfall, potentially lifting regional GDP by 12% or more by 2050. The continent offers scale, diversification and cost advantages in mining and refining, as governments roll out fresh incentives. Investors are especially interested in expansions of existing projects, modular refineries and those mining sites that already have buyers lined up.

Risks:

Challenges include slow permitting timelines, lack of infrastructure and volatile commodity prices. There’s also the question of whether technologies such as chips and electric cars will in the future use the same mix of minerals currently in demand.

Some Countries to Watch:

The Democratic Republic of Congo dominates cobalt output, producing more than 70% of global supply while sitting on half of known reserves. Meanwhile, its lithium potential is barely tapped. South Africa controls most of the world’s manganese resources. Ghana, Mozambique, Namibia, Tanzania and Zambia are also critical mineral countries to watch.

The Key NumberLess than 2%Share of world’s data-center capacity in Africa*

Who’s Investing?

Equinix Inc., Microsoft Corp., Visa Inc.

Investment Case:

Africa’s fast-growing digital economy is fueling strong demand for data centers, as internet use, mobile adoption and cloud migration accelerate. By 2030 mobile-network trade association GSMA expects mobile data traffic per connection in sub-Saharan Africa to quadruple, fueled by wider broadband coverage, cheaper smartphones and the appetite for data-hungry content. Investors are looking beyond big data hubs to facilities that process information nearer to where it’s used. They’re also finding opportunities in cloud services and green-powered facilities. Governments are offering tax incentives, reduced import duties on equipment and streamlined licensing processes to attract foreign direct investment.

Risks:

Energy costs and power supply, plus a lack of clear regulation and efficient cooling systems, are risk areas.

Some Countries to Watch:Mauritius and Egypt have emerged as prime destinations for data-center investment, underpinned by their high GDP per capita, robust mobile adoption and dependable electricity access. Ivory Coast, Kenya, Morocco and South Africa also appeal to investors for their deep mobile penetration and expanding digital infrastructure.

The Key Number60%Africa’s share of the world’s land that would be good for solar panels*

Who’s Investing?

ACWA Power, Engie SA, Scatec ASA

Investment Case:

The continent’s electricity demand is set to double by 2040, creating a massive market for renewables. Investment returns are supported by long-term power purchase agreements, cheap financing from development banks and guaranteed prices for electricity sold to the grid. Growth will be driven by population expansion, urbanization and industrialization, alongside global climate commitments. To attract funding, some governments are offering tax breaks, public-private partnership frameworks, and sovereign or multilateral guarantees to reduce investor risk.

Risks:

Grid integration remains a challenge; so does policy inconsistency in some markets. There’s also a chance demand is lower than projected or buyers don’t honor purchase agreements.

Some Countries to Watch:

Opportunities abound in utility-scale solar and wind, as well as in off-grid and minigrid solutions for electrification, in nations including Botswana, Egypt, Rwanda, Senegal and Zambia. Also watch the emerging green hydrogen space in Morocco, Namibia and South Africa.

The Key Number8%Global share of crude oil production in 2023*

Who’s Investing?

Chevron Corp., Eni SpA, Shell Plc

Investment Case:

Hydrocarbons remain central to many African economies, with oil and gas exports anchoring fiscal revenue. Global primary energy demand is set to climb 18% by 2050, led by Asia Pacific and Africa, according to Gas Exporting Countries Forum’s Global Gas Outlook 2050. Despite the growth of renewables, natural gas will play a longer-term role in meeting the world’s growing energy needs. Tax credits, customs duty exemptions and production-sharing contracts with cost recovery are some of the incentives drawing in investors.

Risks:

Policy uncertainty, potential vandalism of assets and cost of capital are all obstacles to growth.

Some Countries to Watch:Nigeria has emerged as a net exporter of refined products, thanks to the 650,000-barrel-a-day Dangote Petroleum Refinery, which is reshaping fuel markets across West Africa. Uganda also plans to build a refinery. Morocco is building liquefied natural gas import terminals and cross-border gas links, while Egypt plans to increase its oil and gas exploration. In Namibia, offshore discoveries are drawing major companies and could transform the economy.

Investment Case:

The upside is big. In some scenarios, Africa’s manufacturing output could rise to 18% of GDP by 2043, from 13% in 2023, fueled by rising consumer demand and infrastructure spending. That growth would make manufacturing one of the continent’s fastest-expanding investment opportunities, especially as the AfCFTA opens smoother trade channels within the 1.6 billion-person market. Tax breaks, benefits for investments in designated SEZs and better loan terms are all helping attract spending.

Risks:

Africa’s factories promise scale, but policy uncertainties, weak infrastructure, cheap imports, costly power and fragmented markets are holding back a manufacturing boom.

Some Countries to Watch:Morocco has established itself as a continental automotive hub, exporting cars and electric vehicles to Europe. Egypt is building electronics and batteries, and Ethiopia’s industrial parks are attracting apparel and light-manufacturing investments. South Africa remains strong in automotive and capital goods, while Ghana and Nigeria are emerging through SEZ-led agro-processing and consumer goods industries.